Imagine a world where your clients view you not just as a mutual fund distributor, but as a trusted advisor who guides them through every aspect of their financial lives. In today’s ever-changing financial landscape, staying ahead of the curve is essential. The Certified Financial Planner (CFP) certification can make this vision a reality, offering unmatched opportunities to distinguish yourself and advance your career.

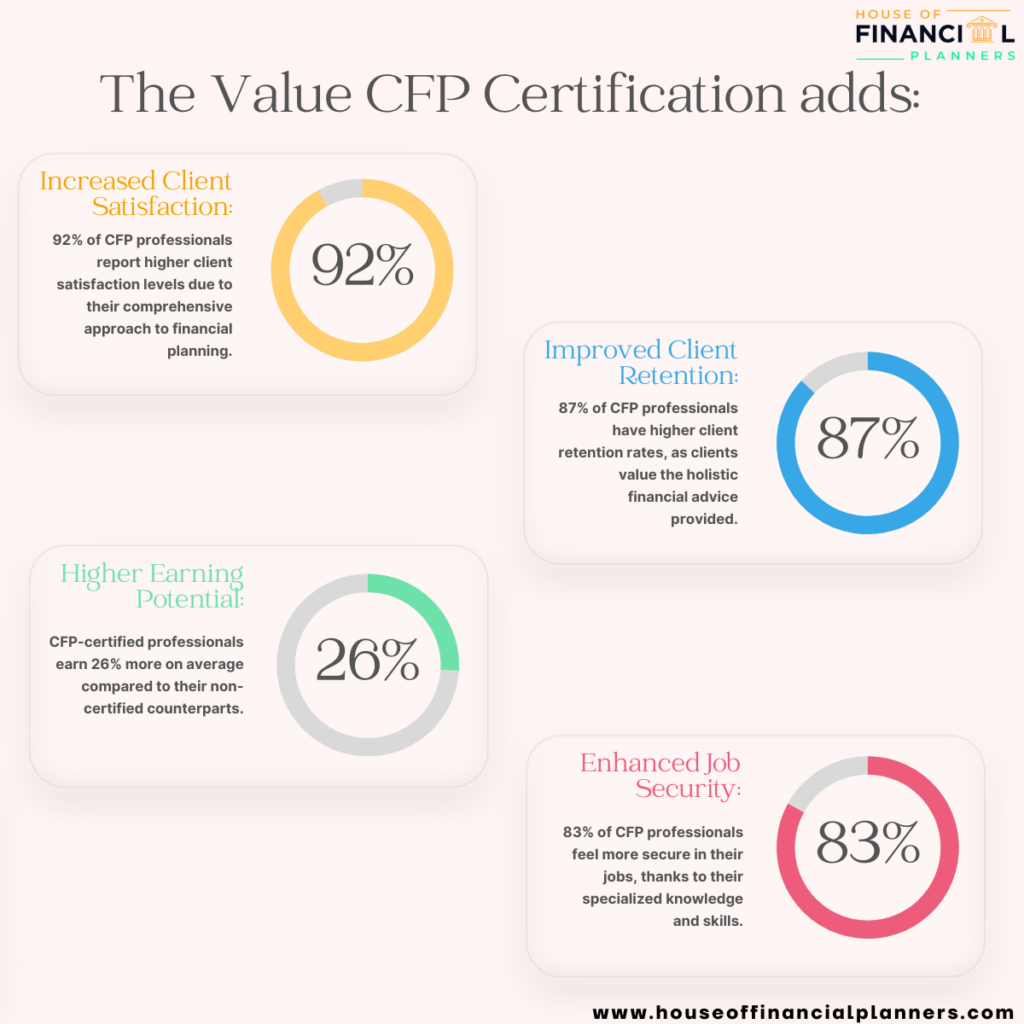

The Value CFP Certificate adds:

FPSB has done the research.

Increased Client Satisfaction: 92% of CFP professionals report higher client satisfaction levels due to their comprehensive approach to financial planning.

Improved Client Retention: 87% of CFP professionals have higher client retention rates, as clients value the holistic financial advice provided.

Higher Earning Potential: CFP-certified professionals earn 26% more on average compared to their non-certified counterparts.

Enhanced Job Security: 83% of CFP professionals feel more secure in their jobs, thanks to their specialised knowledge and skills.

How CFP Certification Can Increase Your Business?

Make Smarter Decisions with Extensive Knowledge

Knowledge is power, and with a CFP certification, you’ll have a treasure trove of it. Imagine having the ability to make well-informed decisions that not only benefit your clients but also grow your business. With a broad knowledge base, you can tackle estate planning and tax planning with ease, leading to more insightful conversations with your clients. This expertise helps you manage more of their assets and builds a larger, more loyal clientele.

Why stop at being just a mutual fund distributor? With CFP certification, you can expand your horizons and offer consulting services, including financial planning, estate planning, and tax planning. These additional services are like adding more strings to your bow, attracting new clients and increasing the value you provide to existing ones. As they say, “Variety is the spice of life,” and offering a variety of services spices up your business, making it more attractive and competitive.

How CFP Certification can help you protect your business?

Secure Your Assets Under Management (AUM)

Ring Fencing:- Imagine building a substantial AUM of 100 crores. Now, picture a competitor with advanced knowledge trying to lure your clients away. Scary, right? As a CFP, you can protect your Assets Under Management (AUM) from such potential threats. This certification equips you with the expertise to safeguard your business, ensuring that your clients’ assets remain with you. It’s like building a fortress around your hard-earned assets, creating long-term trust and stability.

The benefits of getting a CFP certification for mutual fund distributors are crystal clear. It boosts your credibility, builds trust with your clients, increases your earning potential, and provides you with extensive financial knowledge. Additionally, it helps you protect your assets under management (AUM) from future threats, ensuring long-term stability for your business. In short, this certification is a smart investment in your career and future success.

Conclusion

As Benjamin Franklin once said, “An investment in knowledge pays the best interest.” If you’re ready to take your career to the next level, consider pursuing CFP certification. Visit the House of Financial Planners for more information on how to get started. Transform your career, enhance your knowledge, and become the financial expert your clients need today!

Don’t just aim for success; strive for significance in your clients’ lives. Get your CFP certification and make a lasting impact.

The journey after the 12th can be both exciting and daunting, filled with endless possibilities and tough choices. If you have a passion for finance and a desire to shape your future, then the Certified Financial Planner (CFP) course should be at the top of your list.

Let’s take a look at the various popular finance-related courses you could pursue after finishing 12th grade:

Certified financial planning (CFP)

Chartered Accountancy (CA)

Company Secretary (CS)

Cost and Management Accountancy (CMA)

Bachelor of Commerce (B.Com)

Bachelor of Business Administration (BBA)

Bachelor of Economics (BE)

Among these options, the CFP program is particularly noteworthy as it offers a comprehensive entry point into a satisfying and lucrative career in Financial Planning/Personal Finance.

What is CFP and Why Should You Consider It?

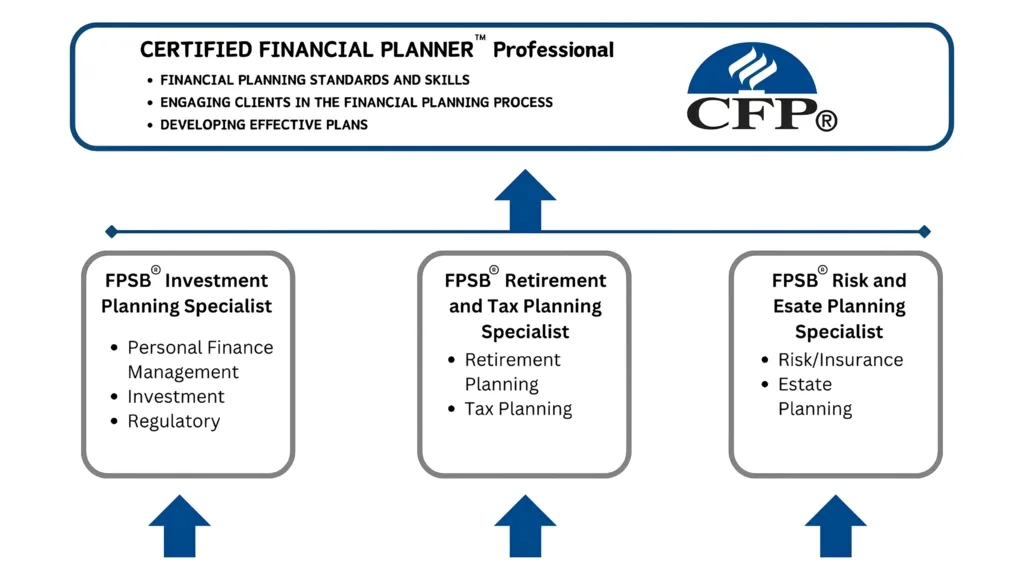

The Certified Financial Planner program is a globally recognized certification that equips you with the knowledge and skills to provide holistic financial planning services. It covers everything from investment planning, tax planning, retirement planning, estate planning, and more. With a CFP certification, you’ll be part of an elite group of professionals who can guide individuals in personal finance. Remarkably, by completing the CFP program, you’ll earn four valuable certifications, setting you apart from the crowd.

Certificates You Will Earn with CFP:

Investment Planning

Risk and Estate Planning

Retirement and Tax Planning

Certified Financial Planner

A major benefit of the CFP certification is its global recognition. Accepted in 27 countries, it allows you to seek international career opportunities and collaborate with financial professionals worldwide, underscoring the program’s excellence and relevance.

One of the key advantages of the CFP certification is its global recognition. The program is currently recognized in 27 countries worldwide, allowing you to explore international career opportunities and collaborate with financial professionals across borders. This global acceptance underscores the program’s excellence and validity, making it a passport to success in the ever-evolving world of finance.

Is CFP right for you?

The beauty of the CFP course lies in its inclusivity. Whether you’re a fresh mind straight out of 12th or a working professional seeking career growth, the program welcomes all. The only prerequisites are a strong numerical aptitude, excellent communication skills, and an unwavering commitment to ethics and client-centricity.

The Future of CFP

As the world becomes increasingly complex, the need for skilled financial planners continues to soar. With people seeking expert guidance to navigate their finances, a CFP certification opens doors to numerous opportunities in banks, investment firms, insurance companies, and independent financial advisory firms. The future is bright, and those who embrace CFP today will be at the forefront of this ever-growing industry.

Why Pursue CFP Immediately After 12th?

While the CFP course is open to all, there are distinct advantages to pursuing it right after 12th:

Head Start: By starting early, you’ll gain a significant head start in your career, allowing you to build experience and expertise while your peers are still completing their undergraduate studies.

Focused Learning: With a fresh and receptive mind, you’ll be able to absorb the complex concepts of financial planning more effectively, laying a solid foundation for your future success.

Early Exposure: The CFP program includes practical training and internships, providing you with invaluable industry exposure and networking opportunities right from the start.

Competitive Edge: As a young CFP professional, you’ll stand out in the job market, showcasing your dedication, foresight, and commitment to excellence.

Advantages of Pursuing CFP After 12th

By choosing to embark on the CFP journey right after the 12th, you’ll unlock a plethora of benefits that will shape your future:

Accelerated Career Growth: With an early start and focused training, you’ll be able to climb the career ladder at a faster pace, opening up opportunities for leadership roles and higher earning potential.

Diverse Career Paths: The CFP certification is a versatile qualification that opens doors to various industries, including banking, insurance, wealth management, and independent financial advisory firms.

Global Recognition: As a CFP professional, you’ll be part of a globally recognized network, enabling you to explore career opportunities worldwide.

Lifelong Learning: The financial world is ever-evolving, and the CFP program ensures that you stay up-to-date with the latest trends, regulations, and best practices through continuous education and professional development.

Personal Fulfillment: As a CFP professional, you’ll have the opportunity to make a tangible difference in people’s lives by guiding them towards financial security and helping them achieve their dreams.

At the House of Financial Ahmedabad, we offer online, offline, and hybrid classes, we believe in empowering young minds to shape their futures and make a lasting impact. Our CFP program is designed to nurture your talents, hone your skills, and prepare you for a fulfilling career in financial planning.

Don’t let the opportunities slip by. Embrace the CFP journey right after the 12th and unlock a world of possibilities. Your future is waiting; it’s time to take the leap and soar to new heights!

Got any doubts? Do check our free workshop page and register for it. Free Workshop

Got any doubts about the fees of CFP? Do check our fee calculator. CFP Cost Calculator

Act now and let’s chart your path to success together!

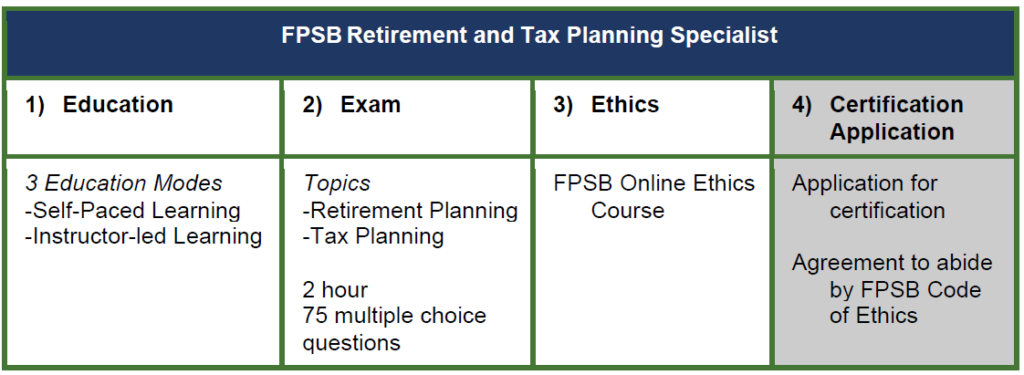

Are you prepared for an excellent educational opportunity provided by Financial Planning Standards Board Ltd.(FPSB), the organization that sets standards for the worldwide financial planning industry? The retirement and tax planning course from FPSB Ltd. can be taken online or with an instructor like House of Financial Planners FPSB Ltd.’s retirement and tax planning course helps you create strategies to increase your clients’ wealth and manage their money better as they approach and go through retirement. It also guides you how to use tax planning to help achieve their goals.

The course teaches you to take into account your client’s individual financial objectives, risk capacity and tolerance, asset locations, the composition and effects of public and private retirement plans, and the effects of taxes on your clients’ financial status and objectives. To gain recognition from employers, clients, and the public for your expertise in retirement and tax planning, follow the steps outlined below to achieve the FPSB Retirement and Tax Planning Specialist certification in India.

About FPSB Ltd. and FPSB Programs in India

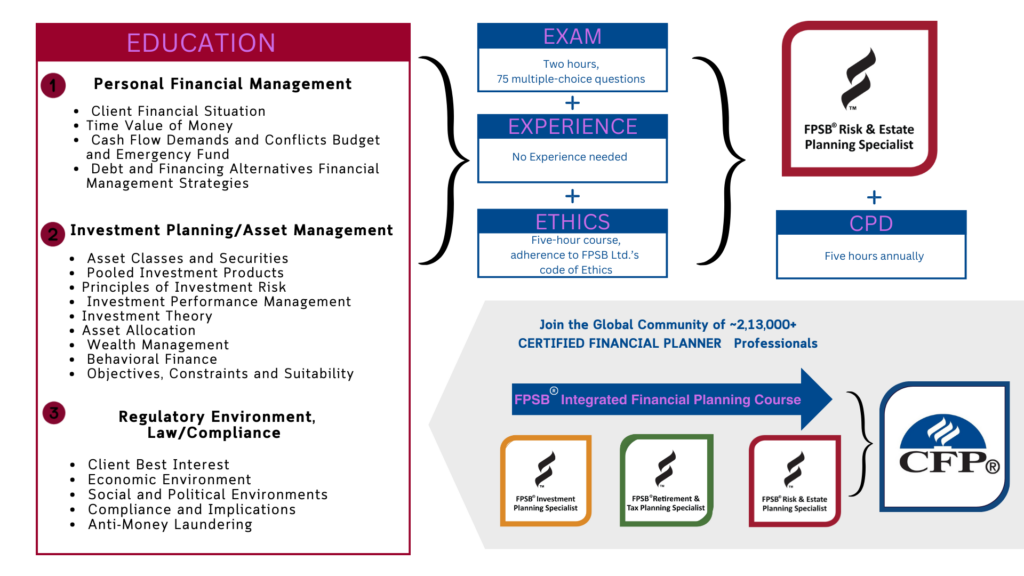

The Financial Planning Standards Board Ltd. (FPSB) sets global standards for financial planning and owns the CFPCM, CERTIFIED FINANCIAL PLANNERCM and marks outside the United States. FPSB proudly offers FPSB’s Retirement and Tax Planning Specialist program, which is one of three pathways to achieving CFP certification in India:

FPSB® Investment Planning Specialist

FPSB® Risk and Estate Planning Specialist

FPSB® Retirement and Tax Planning Specialist

Each certification pathway has specific requirements, including coursework, exams, and credentials. Notably, completing FPSB’s pathways also counts towards the educational requirements needed for CFPCM certification in India. Professionals interested in pursuing CFP certification can start by enrolling with FPSB for any of these three pathway certifications in any sequence. This blog will specifically address the FPSB Retirement and Tax Planning Specialist certification.

FPSB® Retirement and Tax Planning Specialist Overview

Take Your Career to the Next Level

Available online or through an instructor like House of Financial Planners, the FPSB® Retirement and Tax Planning Specialist course equips you to create strategies that enhance your clients’ wealth and cash flow as they approach and enter retirement, and it provides guidance on incorporating tax planning to support their objectives.

This course instructs you to analyze your clients’ personal financial goals, their risk tolerance and risk capacity, asset allocation, the structure and impact of public and private retirement plan, and how taxation will affect your clients’ financial situation and goals. To gain recognition from employers, clients, and the public for your advanced expertise in retirement and tax planning, follow the steps provided below to earn your FPSB® Retirement and Tax Planning Specialist certification in India.

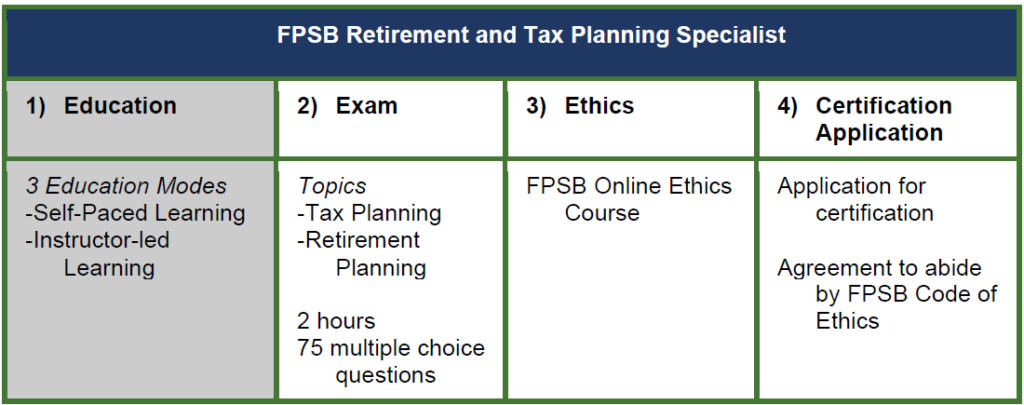

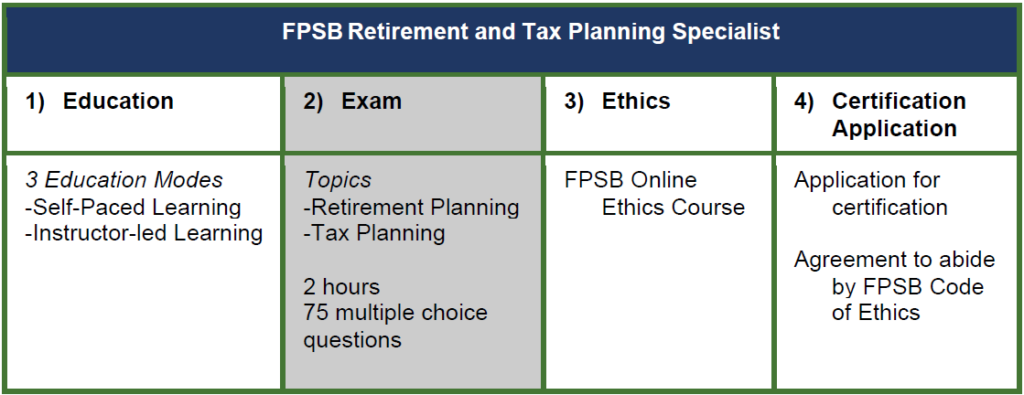

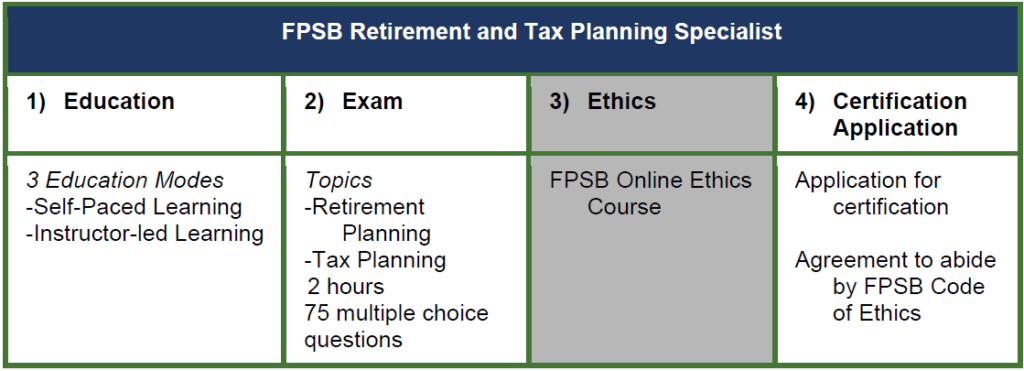

Steps to Initial Certification

The requirements for FPSB® Retirement and Tax Planning Specialist certification are as follows:

Successfully complete the FPSB Ltd. Ethics Course.

Pass the FPSB® Retirement and Tax Planning Specialist exam, which aligns to the topics identified in the FPSB Retirement and Tax Planning Specialist Competency Profile

Complete your certification application, which includes your agreement to comply with FPSB Ltd.’s Code of Ethics and payment of an annual certification fee.

Step 1: Education

Criteria to Register

Candidates must be at least 18 years old and have completed HSC/12th grade (Std XII/HSC) to enroll with FPSB and start the FPSB Retirement and Tax Planning Specialist education course. It is required that candidates register with FPSB at least 30 days before registering for the exam.

Period for Course Completion

Individuals are required to finish the FPSB® Retirement and Tax Planning Specialist certification program within three years from their initial registration with FPSB Ltd. and must renew their registration every year. If the program is not completed within three years, FPSB Ltd. will deem the registration invalid. Candidates should evaluate their ability to meet this timeline before registering.

FPSB Ltd. Educational Resources

FPSB Ltd. will provide program participants with digital textbooks, supplementary post-chapter quizzes, post-module exams, and additional course materials via its online learning platform, MyFPSBlearning. All educational resources provided by FPSB Ltd. are tailored to the FPSB Retirement and Tax Planning Specialist learning. Every candidate, irrespective of their chosen method of study, must acquire these materials.

Education

Candidates may complete the FPSB® Retirement and Tax Planning Specialist education requirement and become eligible to sit for the certification exam in one of three ways:

1. Self-Paced Education

Candidates who sign up with FPSB and choose the “Self-Paced Learning” option will be given a password to access FPSB’s online learning portal, MyFPSBlearning. There, they can study and interact with various FPSB learning materials at their own pace, and evaluate their understanding through quizzes and module tests, enhancing their learning experience. This self-directed educational path may be especially suitable for appealing to experienced investment professionals or self-starters who enjoy studying on their schedule.

*Self-paced learners who do not pass all FPSB Retirement and Tax Planning Specialist module exams within two attempts, they will be required to switch to the instructor-led method by registering with an Authorized Education Provider (AEP). The House of Financial Planners is one of the AEP’s of FPSB

2. Instructor-Led Education

Candidates seeking a comprehensive educational experience with interactive learning and access to an FPSB Authorized Education Provider should choose the “Instructor-Led Learning” option when registering with FPSB. FPSB Authorized Education Providers deliver both classroom and online learning experiences. Upon registering for instructor-led education with FPSB, individuals will be prompted to choose from among FPSB’s authorized providers, all of which are detailed on the FPSB Ltd. website.

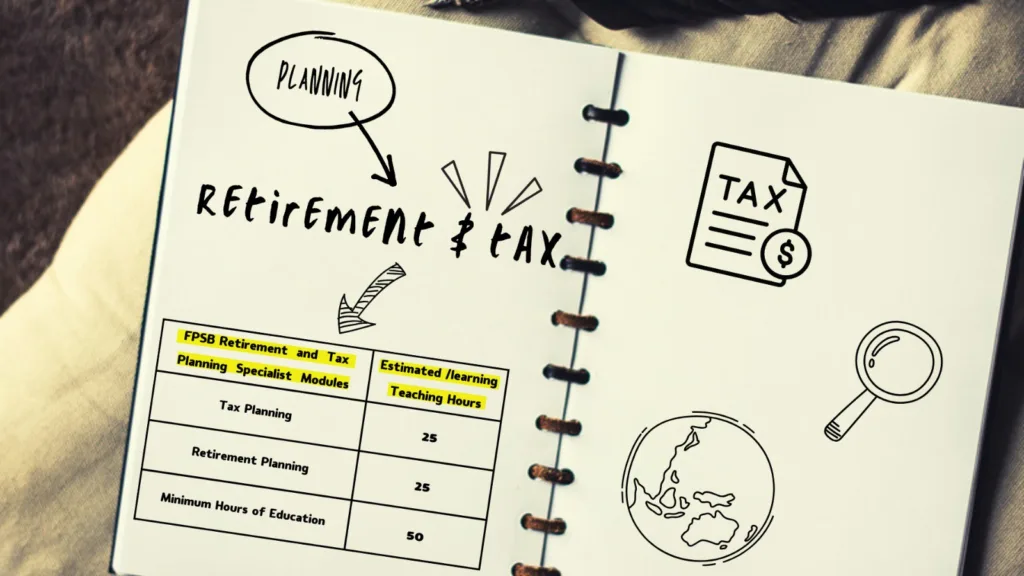

Candidates who opt for FPSB’s instructor-led education can expect to receive the below teaching hours per module.

Step 2. Exam

After successfully finishing the FPSB Retirement and Tax Planning Specialist education requirement, either through instructor-led options like House of Financial Planners or via a self-paced education course, candidates will be eligible to take the FPSB® Retirement and Tax Planning Specialist exam.

This exam evaluates the knowledge, skills, and abilities required to obtain the FPSB® Retirement and Tax Planning Specialist credential. It focuses on the essential functions of collection, analysis, and synthesis, which are further elaborated below. Each exam question primarily targets a specific competency element outlined in the FPSB Retirement and Tax Planning Specialist Competency Profile and might involve integrating multiple competencies.

Exam Overview

75 multiple-choice questions (4 possible answer choices), of which a minimum of 65 questions are potentially scored and up to 10 questions are used to develop future exams.

Computer-based testing format

Duration – two hours

Financial calculators permitted (data must be erased)

There will be two possible marks: correct, with points allotted; or incorrect, for zero points. Candidates will not have points deducted (referred to as ‘negative marking’)

Exam Scoring

The passing point on the FPSB® Retirement and Tax Planning Specialist exam is set to a level that is what is required for competent practice. Once set, future exams are equated to this same level so that candidates who take the exam one month have the same opportunity to demonstrate their abilities as candidates who take the exam a different month. The level of ability is what is consistent. This means that even if one exam is harder than another, the equating process gives every candidate the same opportunity to pass.

Areas of Practice

The exam will test the following areas of practice, which are also described to in more detail in the FPSB Retirement and Tax Planning Specialist Competency Profile.

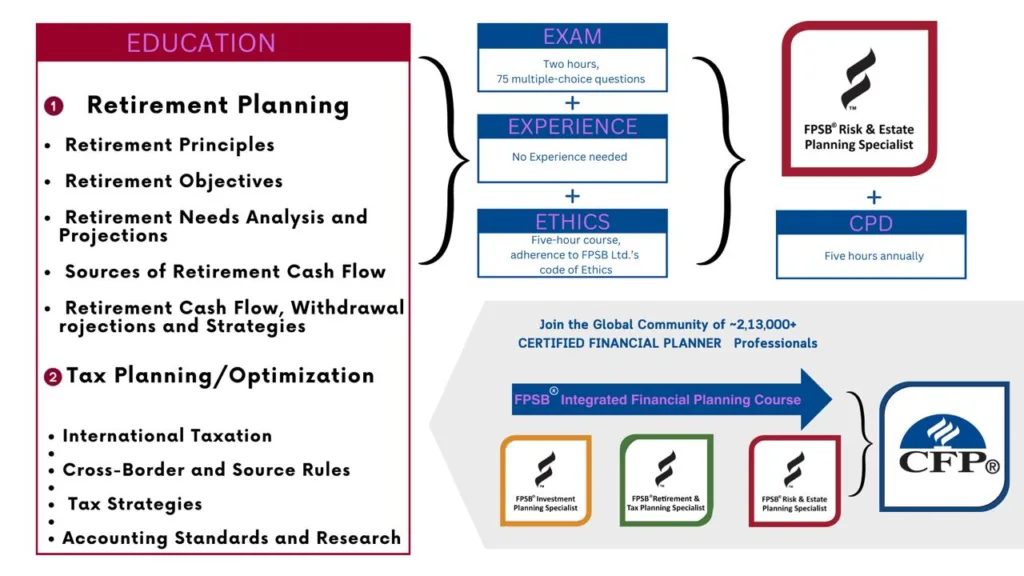

FPSB Retirement and Tax Planning Specialist Areas of Practice

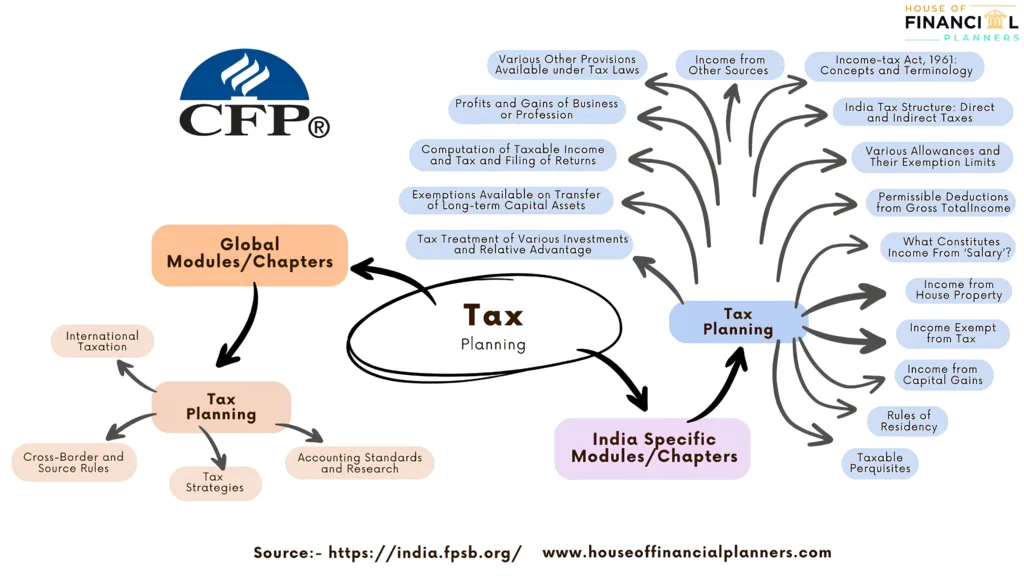

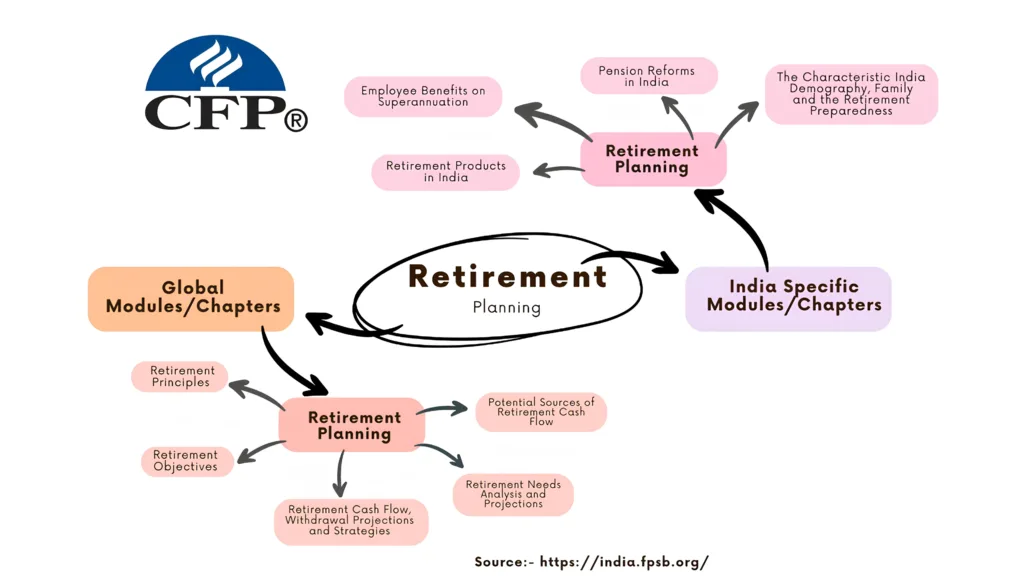

Retirement Planning 1. Retirement Principles 2. Retirement Objectives 3. Retirement Needs Analysis and Projections 4. Potential Sources of Retirement Cash Flow 5.Retirement Cash Flow, Withdrawal Projections and Strategies

Tax Planning 1. International Taxation 2. Cross-Border and Source Rules 3. Tax Strategies 4. Accounting Standards and Research

India Specific Modules/Chapters

Retirement Planning

Tax Planning

1. The Characteristic India Demography, Family, and the Retirement Preparedness 2. Pension Reforms in India 3. Retirement Products in India 4. Employee Benefits on Superannuation

1. India Tax Structure: Direct and Indirect 2. TaxesIncome-tax Act, 1961: Concepts and Terminology 3. Rules of Residency 4. What Constitutes Income From ‘Salary’? 5.Various Allowances and Their Exemption Limits 6. Taxable Perquisites 7. Income from House Property 8. Income from Capital Gains 9. Income from Other Sources 10. Income Exempt from Tax 11. Exemptions Available on Transfer of Long-term Capital Assets 12. Permissible Deductions from Gross Total Income 13. Profits and Gains of Business or Profession 14. Tax Treatment of Various Investments and Relative Advantage 15. Various Other Provisions Available under Tax Laws 16. Computation of Taxable Income and Tax and Filing of Returns

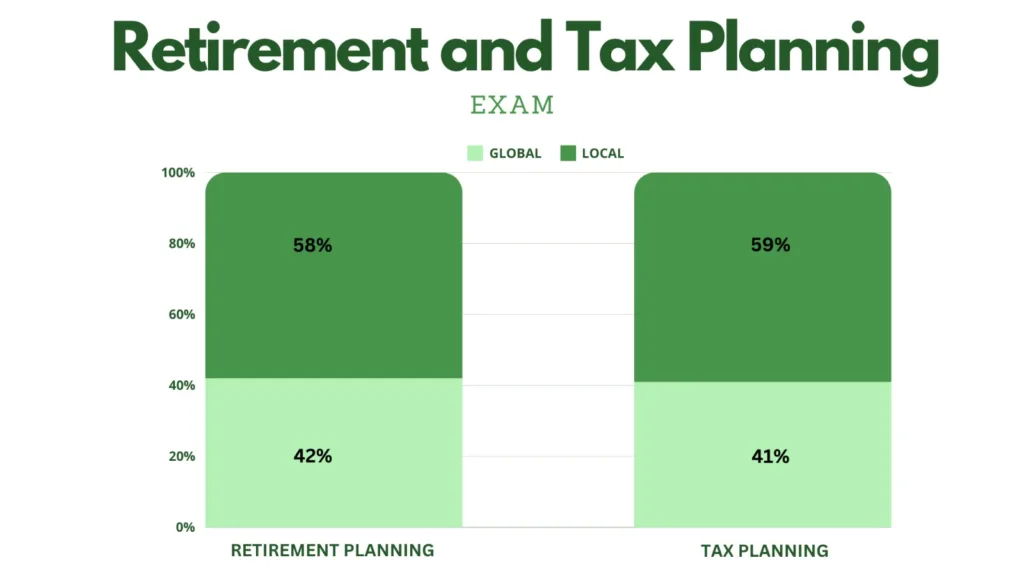

The FPSB Retirement and Tax Planning Specialist exam will test the knowledge, skills and abilities from the FPSB Retirement and Tax Planning Specialist education modules in the below proportions. However, there will not be specific sections allocated to the modules. Instead, questions relating to each module will appear in no specific order throughout the exam.

Likewise, although the FPSB Retirement and Tax Planning Specialist textbooks draw a distinction between “global” and “India-specific” education content, exam questions will not be specifically identified as such, and will appear in no specific order throughout the exam.

Difficulty Levels

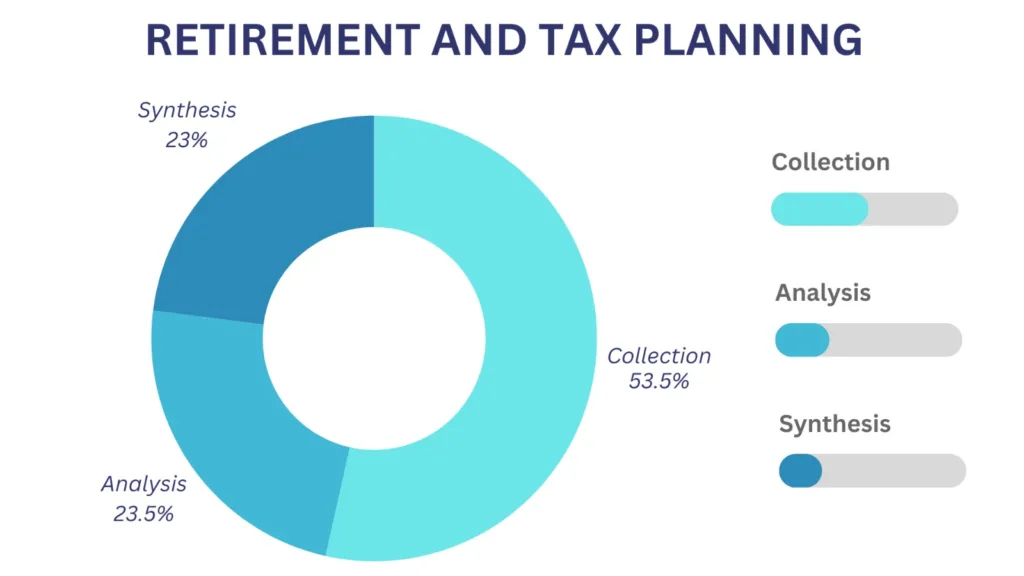

The FPSB Retirement and Tax Planning Specialist certification exam is designed to assess knowledge, skills and abilities in the areas of collection, analysis and synthesis in approximately the following proportions:

Collection: Gathering information and identifying related facts by making required calculations and arranging client information for analysis. During the collection function, the core competency is to collect both the quantitative and qualitative information required to provide retirement advice.

Analysis: Considers issues, performs financial analysis and assesses the resulting information to be able to develop strategies for the client. This includes: (1) considering potential opportunities and constraints in developing strategies, and (2) assessing information to develop strategies.

Synthesis: Integrates the information needed to develop and evaluate strategies to create a retirement plan.

Once submitted, exam results will be reviewed in detail and the Candidate will receive additional determination information. Any appeal must be received no later than 30 days from the intimation of the exam result in LMS or through email. The decision after the appeal is completed will be considered final.

Step 3. Ethics

FPSB mandates that all individuals complete the FPSB Ethics course shortly after registering for the FPSB® Retirement and Tax Planning Specialist course. This course, included with the course materials purchase, is crucial as passing it and adhering to the Code of Ethics are prerequisites for obtaining the FPSB® Retirement and Tax Planning Specialist certification. The requirement to pass the Ethics course applies only once, even if pursuing multiple Specialist certifications and the CFPCM certification. Conducted online via MyFPSBlearning, the FPSB Ethics Course features interactive, recorded lessons that can be completed in one or several sessions, with periodic knowledge assessments. Once finished, this course fulfills the ethics training requirement for all FPSB Ltd. certifications available in India.

Ethics Attestation

After candidates have passed the FPSB Ethic Course, they must, as part of the FPSB Retirement and Tax Planning Specialist certification process, attest and agree to abide by the FPSB Code of Ethics.

1. Evaluate the public perception of the financial services profession

Knowledge Items

1. Why financial services professionals should study ethics 2. The difference between values and principles 3. Ethics and the law 4. Characteristics of a financial services professional 5. Public perception of the financial services profession

1. Construct a personal code of ethics

Knowledge Items 1. The purpose of a code of ethics 2. Business conduct standards 3. Reasonable person standard 4. Professional practice standard 5. Eight principles of FPSB’s Code of Ethics 6. Personal code of ethics

Step 4. Initial and Ongoing Certification

Ongoing Certification Requirements

To retain the FPSB Retirement and Tax Planning Specialist credential, certification holders are required to continually update their professional skills, knowledge, and competencies through ongoing educational activities.

FPSB Ltd. mandates that FPSB Retirement and Tax Planning Specialists renew their certification every year. To remain certified, you must:

✔ Commit to adhere to FPSB Ltd.’s Code of Ethics and any applicable laws and regulations.

✔ Obtain at least five Continuing Professional Development (CPD) hours/points. All points must be completed before applying for renewal of certification. At least two CPD hours/points need to directly relate to FPSB Ltd.’s Code of Ethics.

FPSB Coursework as Continuing Professional Development

FPSB Retirement and Tax Planning Specialists who pursue other Specialist courses are considered to have met their annual CPD requirement through the coursework for FPSB’s other financial certifications – as proven by registration in the FPSB Risk and Estate Planning Specialist, FPSB Investment Planning Specialist, or CFPCM certification programs.

Using your Badge and Certification Name Correctly

FPSB will post guidance on how to correctly identify yourself as an FPSB Retirement and Tax Planning Specialist. All certification holders will be required to abide by the guidance as part of the FPSB Code of Ethics.

FPSB Retirement and Tax Planning Specialist Competency Profile Module:

Retirement Planning

Global Retirement Planning

Chapter 1: Retirement Principles

Learning Objectives

1-1 Explain the value of planning for retirement

1-2 Analyze strategies for funding retirement

Knowledge Items

1.1 Value of early and consistent planning for retirement

1.2 Investing for retirement

1.2.1 Accumulation strategies

Chapter 2: Retirement Objectives

Learning Objectives

2-1 Identify a client’s retirement objectives

2-2 Evaluate the implications of a client’s attitudes toward retirement

2-3 Evaluate trade-offs needed to meet a client’s retirement objectives

2-4 Calculate capital required to fund a client’s retirement

Knowledge Items

2.1 Retirement goals and objectives

2.1.1 Goals and needs

2.1.2 Capital required for retirement

2.1.3 High net worth clients

2.2 Establishing retirement cash flow targets

2.2.1Conflicting goals and trade-offs

2.3 Objectives in retirement

2.4 Wealth transfer

Chapter 3: Retirement Needs Analysis and Projections

Learning Objectives

3-1 Identify the types of information to collect regarding a client’s estimated retirement expenses 3-2 Analyze financial goals and obligations

3-3 Calculate financial projections in retirement based on a client’s current financial position 3-4 Calculate amounts required to fund retirement cash flow needs

3-5 Analyze the impact of changes in assumptions on financial projections

Knowledge Items

3.1Longevity risk, inflation and the impact on retirement cash flow needs

3.2 Goal classification and funding

3.2.1 Fixed and terminable

3.2.2 Fixed and permanent

3.2.3 Variable and terminable

3.2.4 Variable and permanent

3.3 Goal development

3.3.1 Establishing goals and timelines

3.3.2 Determining goal priorities

3.4 Selecting and administering long-term investment portfolios

3.4.1 Risk, return and implications for retirement planning

Chapter 4: Potential Sources of Retirement Cash Flow

Learning Objectives

4-1 Identify details to collect of a client’s potential retirement cash flow sources

4-2 Analyze retirement benefits provided by the government

4-3 Analyze retirement benefits provided by employers

4-4 Explain how annuities are used to provide retirement cash flow

Knowledge Items

4.1 Pension funds

4.1.1 Government-sponsored

4.1.1.1 Defined benefit plans

4.1.2 Employer-sponsored

4.1.2.1 Defined contribution plans

4.2 Types of non-pension employee retirement benefits

4.3 Individual retirement plans

4.4 Annuities

4.4.1 Types of annuities

4.4.2 Settlement and payout options

Chapter 5: Retirement Cash Flow, Withdrawal Projections and Strategies

Learning Objectives

5-1 Calculate and analyze financial projections for a client’s retirement plan.

5-2 Describe whether a client’s retirement objectives are realistic

5-3 Describe the impact of changes in assumptions on financial projections

5-4 Calculate, analyze, and explain factors impacting retirement account distributions.

5-5 Apply retirement distribution strategies

Knowledge Items

5.1 Sources of cash flow in retirement

5.2 Portfolio distribution strategies

5.3 Retirement distribution rates

5.4 Sequence risk

5.4.1 Portfolio distribution options

5.5 Impact of taxes on retirement cash flow

India-Specific Retirement Planning

Chapter 1: The Characteristic India Demography, Family and the Retirement Preparedness

Learning Objectives

1-1 Understand India demography and potential disruptions in the future

1-2 Compare fiscal constraints with social security programs

1-3 Explain characteristics of the Indian family unit

Topics

1.1. A young India with low old age dependency ratio

1.2 Improving Life Expectancies, other Potential Disruptions to India Demography

1.3 Fiscal Constraints to deal with Large-scale Social Security Programs

1.4 A typical Indian Family – Three generations living together is still more common

1.5 Other Priority Goals and Obligations delay or disrupt retirement savings

1.6 Late Marriages and subsequent goals blur usual Life Stages

Chapter 2: Pension Reforms in India

Learning Objectives

2-1 Explain Old Age Social and Income Security (OASIS) Project

2-2 Distinguish pension scenario and defined benefit schemes

Topics

2.1 Old Age Social and Income Security (OASIS) Project

2.2 Pension Scenario – State Governments, Autonomous Bodies and Un-organized Sector

2.3 Government – Decisive shifting away from Defined Benefit Schemes

2.4 Mandatory contributory system

Chapter 3: Retirement Products in India

Learning Objectives

3-1 Understand employee provident funds and their digital transition

3-2 Illustrate National Pension System’s (NPS) infrastructure, functioning and advantages

3-3 Explain Public Provident Fund (PPF) and other voluntary institutional retirement products

3-4 Evaluate annuities and reverse mortgage schemes

Topics

3.1 Provident Funds

3.1.1 Employees’ Provident Fund and Employees’ Pension Scheme

3.1.2 Other recognized Provident Fund Types

3.1.3 Defined Contribution Plans – Institutional Framework and Investment Architecture

3.1.4 Tax Benefits on Subscriptions and Withdrawals

3.1.5 Universal Account Number (UAN) and Employer Portability

3.2 National Pension Systems (NPS) – PFRDA (Pension Fund) Regulations, 2015

3.2.1 Signature Scheme of Pension Fund Regulatory and Development Authority (PFRDA)

3.2.2 Unique Permanent Retirement Account Number (PRAN) and Portability Features

3.2.3 Types of Accounts – Tier-I and Tier-II

3.2.4 Tier-I Account (Meant for retirement savings)

3.2.4.1 Tax Treatment – Exempt-Exempt-Taxed (EET)

3.2.4.2 Withdrawal Limits on Retirement, Taxability and other Rules

3.2.4.3 An Exclusive Additional Tax Deduction under Section 80CCD(1B)

3.2.4.4. Other Features – Very Low Cost, Regulated and Funds based (Accumulated Units)

3.2.4.5 Annuity Provisions and Annuity Service Providers (PFRDA empaneled)

3.2.4.6 Partial withdrawal, Premature withdrawal, continuation and deferment

Broad Principles that categorize ‘Income’, Extended meaning of income

Capital and Revenue Receipts, and their Taxability

Chapter 3: Rules of Residency

Learning Objectives

3-1 Illustrate norms that establish the tax status of residents

3-2 Determine factors which differentiate Indian income from foreign income

Topics

Residential status of an individual and other taxable entities

Taxability based on Residential status

Individuals – Resident in India, Ordinarily Resident and Not-ordinarily resident

Individuals – Not-resident in India (NRI)

Residential Status of a Foreign Company

Residential Status of Hindu Undivided Family (HUF)

Residential Status of ‘any other person’

Incidence of Tax or Tax Liability

Indian Income and Foreign Income

Income ‘received’ vs. ‘accrue’ or ‘arise’ in India

Income deemed to accrue or arise in India

Chapter 4: What Constitutes Income From ‘Salary’?

Learning Objectives

4-1 Describe salary received in various forms and under various heads

4-2 Distinguish all receipts which are recognized and taxed within the meaning salaries

Topics

Salary received, salary due, arrears of salary, advance salary

Various heads of salary and their taxability

Various allowances including Dearness Allowance

Various perquisites

Profits in lieu of salary

Wages

Fees and Commission

Gratuity, Exemption limits – Government and other employees – on retirement or resignation

Annuity and Pension – Taxability of commuted pension amount – received with or without Gratuity payment

Leave encashment on retirement or resignation

Balance in recognized Provident Fund

Employer contribution under notified pension scheme, National Pension System (NPS) and recognized Provident Funds

Compensation received on Voluntary Retirement/Separation Schemes – Exemption limits for IT commissioner approved VRS/VSS schemes

Chapter 5: Various Allowances and Their Exemption Limits

Learning Objectives

5-1 Distinguish allowances which are exempt subject to rules and limits based on actual expenditure

5-2 Identify the rules and limits for various other specific allowances

Topics

Based on expenditure incurred

House Rent Allowance (HRA)

City Compensatory Allowance

Entertainment Allowance

Special Allowance – Travelling, Conveyance, Daily, Uniform, etc.

Irrespective of expenditure incurred

Hill area allowance

Tribal area allowance

Transport allowance

Chapter 6: Taxable Perquisites

Learning Objectives

6-1 Describe amenities and facilities provided by employer which attract tax

6-2 Illustrate Sweat equity and Employee Stock Options as perquisites and their tax incidence

Topics

Furnished /Unfurnished accommodation with no rent/concessional rent charged

Services of house help, attendant

Supply of amenities (electricity, water, gas, etc.)

Interest free loan or concessional loan

Use of car and other movable assets

Medical facility and club facility

Employer’s contribution towards superannuation fund (above the exempt maximum limit)

Value of specified security, sweat equity, Employee Stock Option Plan (ESOP) allotted/transferred to employee

Tax of an employee paid by employer

Chapter 7: Income from House Property

Learning Objectives

7-1 Evaluate the income ascribed to a house property treated as investment

7-2 Calculate loss from a self-occupied house property built on borrowed capital

Topics

The Basis of Charge

The Basis of computing income from a let out house property

Gross Annual Value (GAV) on the basis of Municipal Valuation (MV), Fair Rent (FR) and Standard Rent (SR)

Net Annual Value (NAV)

Standard Deduction under section 24(a) and Interest on borrowed capital u/s 24(b)

Self-occupied house purchased/built on borrowed capital

Chapter 8: Income from Capital Gains

Learning Objectives

8-1 Categorize various capital assets on their respective norms of long-term holding

8-2 Identify capital assets where the benefit of indexation is not allowed

8-3 Determine cost of acquisition and holding period on transfer of capital assets acquired at no consideration

8-4 Assess capital gain on transfer/redemption of equity oriented and debt securities

Topics

‘Capital Asset’

‘Short-term’ and ‘Long-term’ capital asset

Minimum period for different capital assets to become long-term capital assets

Indexation benefit basis cost inflation index (CII) in respect of certain capital assets

Capital assets transferred under a Gift, a Will, by succession/inheritance, etc. – Basis of cost of acquisition including improvement cost

Fair Market Value for capital assets acquired before April 1, 2001

Capital gain on transfer of land and building

Self-generated capital assets (goodwill, business rights/permits/licenses, trade mark, brand, etc.

Shares converted from debentures/bonds – basis of cost and period of holding

Transfer of securities in Dematerialized form – FIFO basis of cost and period of holding

Transfer of ESOP – cost of acquisition/consideration

Capital gain (long-term) on transfer/redemption of equity shares of domestic companies and units of equity-oriented MF schemes w.e.f. April 1, 2018 (grandfathering provisions)

Capital gain on buyback of shares

Capital gain on transfer/redemption of debt securities and units of income/liquid MF schemes

Tax on long-term/short-term capital gains where Securities Transaction Tax (STT) is paid

Tax on long-term/short-term capital gains where STT is not paid

Chapter 9: Income from Other Sources

Learning Objectives

9-1 Categorize various receipts which have treatment of tax at marginal rates

9-2 Calculate the tax incidence the recipient has on gifts of cash/kind, movable and immovable assets

Topics

Interest on Deposits (with banks, post office, companies, cooperative societies, etc.)

Interest on loans

Interest on securities, e.g. bonds, debentures, government securities, etc. (other than dividend from Indian companies)

Dividends received by residents and ordinarily residents from non-domestic companies

Gifts

Gift of cash and kind exempt within prescribed limit

Gift of movable assets above the prescribed limit

Gift of immovable assets at inadequate consideration

Winning from lotteries, horse races, card games, crossword puzzles, TV shows/contests, etc.

Income from racing establishment

Rental income on letting out plant, machinery, furniture and attached premises to such plant

Advance money received and forfeited in the course of negotiations on transfer of a capital asset

Income from undisclosed sources

Chapter 10: Income Exempt from Tax

Learning Objectives

10-1 Distinguish various income receipts exempt with their respective limits under rules

10-2 Analyze the exemption of Agricultural income and its evaluation on aggregate and net basis

10-3 Illustrate exemption admissible under house rent allowance in various conditions

Topics

Agricultural Income (meaning and tax treatment)

Family income received by a member of HUF

Leave Travel Concession (LTC)

Gratuity received by an employee on retirement or by dependents on death of employee (subject to rules)

Commuted value of pension (subject to rules)

Leave Encashment including on retirement (subject to rules)

Voluntary retirement/separation compensation (subject to rules and limits)

Life insurance policy proceeds1

Amount received on maturity from Public Provident Fund, statutory Provident Fund, Sukanya Samriddhi Scheme

House Rent Allowance (subject to rules and limits)

Income of minor child (subject to limits)

Dividends from domestic companies and Units of Mutual Fund schemes (on or after April 1, 2003, subject to limits w.e.f. April 1, 2018)

Any amount received in a transaction of reverse mortgage (lump-sum or installments)

Chapter 11: Exemptions Available on Transfer of Long-term Capital Assets

Learning Objectives

11-1 Construct a scenario of availing exemption of long-term capital gains arising from transfer of house property

11-2Assess various situations to minimize long-term capital gains on transfer of other capital assets

11-3 Describe the stipulations/conditions to be maintained over various timelines if exemption of long-term capital gains availed

Topics

Capital gains arising from transfer of residential property (long-term)

In acquiring another housing property (in terms of Section 54)

In acquiring Equity shares in an ‘eligible company’2 (in terms of Section 54GB) until March 31, 2021

Capital gains deposit account scheme is utilized to park funds to be used in specified time limits

Capital gains arising from transfer of any long-term capital asset

In acquiring certain specified bonds3 (in terms of Section 54EC)

In acquiring certain long-term specified assets4 (in terms of Section 54EE)

In acquiring the first residential property (in terms of Section 54F)

Chapter 12: Permissible Deductions from Gross Total Income

Learning Objectives

12-1 Categorize deductions from gross total income and optimize them within overall limits

12-2 Evaluate deductions available with short-term and long-term commitments to reduce tax incidence within income constraints and financial goals

Topics

Standard Deduction

Professional Tax

Employer contributions (forming part of Employee cost to company) to statutory and recognized Provident Funds, National Pension System (subject to approved limits)

Approved investments, PF/NPS employee contributions, insurance premium, repayment of borrowed capital in housing loans, etc. (subject to limits of Section 80CCE)

Additional contribution under NPS (subject to limits of Section 80CCD[1B])

Interest on borrowed capital in housing loans (subject to limits of Section 24b)

Medical Insurance premium (Section 80D)

Medical treatment (Section 80DD/Section 80DDB)

Approved Donations (Section 80G)Rent paid by self-employed individuals (subject to rules and limit under Section 80GG)

Interest on deposits in savings bank account (subject to limit under Section 80TTA)

Rebate under Section 87A

Chapter 13: Profits and Gains of Business or Profession

Learning Objectives

13-1 Describe businesses and their receipts with related principles for recognition

13-2 Understand allowances and specific deductions available to businesses

Topics

Meaning of business, profession or vocation

The basis of charge

Business income, profits, compensation received, etc.

Principles for arriving at business income

Exclusions from business income

MAT and AMT – Objectives, Provisions and Applicability

Methods of Accounting

Business allowances and deduction including specific deductions

Depreciation allowance (methods, rates for different assets, set off and carry forward provisions)

Masala Bonds, FCCB, Security Receipts, PTCs, GDRs and Warrants

Tax Applicability on Stock Lending/Borrowing, Segregated portfolios of MFs, Winding up of MF schemes

Sovereign Gold Bonds (SGB), tax advantage on maturity and secondary market transactions over bullion investment

Taxability of Investment Instruments – EEE, EET and ETE

Tax Aspects of AIFs, REITs and InvITs, Derivatives on Currency, Interest Rate and Commodities

Tax Liability on Foreign Investments by NRIs and PIOs

Chapter 15: Various Other Provisions Available under Tax Laws

Learning Objectives

15-1 Explain various provisions under tax laws as well as certain requirements for effective discharge of tax statuses

15-2 Understand and interpret various set-off and carry forward of losses available under various heads as well as loss avoidance not available in dividend and bonus stripping

Topics

Clubbing of Income

Set off and carry forward of losses

Business loss and depreciation

Speculation loss

Capital loss (rules for long-term and short-term set off)

Loss from house property

Loss on sale of shares/securities where dividend received (Section 94[7])

Loss on sale of units of Mutual Fund where bonus units received (Section 94[8])

Deduction and Collection of Tax on Source

Tax Deducted at Source (TDS)

Salaries, Fees on Professional and Technical Services

Rents and Deposits

Payment to Contractors/sub-contractors

Winning from Lotteries, Races, Crossword Puzzles, TV shows/contests, etc.

Withdrawal from provident funds within minimum prescribed period

Tax Collected at Source (TCS)

Penalty in case of failure to deduct TDS/TCS

Rounding off of taxable income

Cash payment over a specified limit

Chapter 16: Computation of Taxable Income and Tax and Filing of Returns

Learning Objectives

16-1 Explain the process to arrive at taxable income and determine tax liability

16-2 Arrange ways to discharge tax liability estimated by way of self-assessment tax and periodical advance taxes

16-3 Understand nuances of timely filing tax return and the associated advantages and as well as pitfalls on default of filing return

16-4 Explain the circumstance where revised return needs to be filed

Topics

Income from all sources

Set off of losses – Current year and earlier years – Gross Total Income

Admissible deductions – Net Income or Taxable Income

Tax Liability – Income taxable at special rates and normal rates

Tax as per slabs and applicable rates, surcharge and cesses

Self-assessment tax

Advance Tax – Due dates of filing and percentage limits of advance tax payable

Who should file Returns?

Exemption Limits for Resident, Senior Citizen and Super Senior Citizen

Benefit of filing Return – Set off of carry forward losses, adjustment/refund of TDS amounts

Appropriate Income Tax Return (ITR) Form

Mode of submission (e-filing) and last due date

Return filed beyond time – Penalty and other consequences

Interest payable on default in furnishing return and default in payment of advance tax

Revised Return

Tax Refunds

FPSB Certification Code of Ethics (for all FPSB certifications)

FPSB LTD. CODE OF ETHICS

Observing the highest ethical and professional standards allows professionals to serve the interests of clients and promote the profession for the benefit of society. As part of their commitment, professionals should provide appropriate disclosures and comply with ethical standards when delivering advice to clients. FPSB has incorporated ethical behavior and judgment, and compliance with ethical standards, into its global standards for professionals. To ensure these obligations are understood, FPSB incorporates ethical standards into its certification requirements.

FPSB’s Code of Ethics Principles are statements expressing in general terms the ethical standards that professionals should adhere to in their professional activities. The comments following each Principle further explain the intent of the Principle. The Principles are aspirational and are intended to provide guidance for professionals on appropriate and acceptable professional behavior.

FPSB’s Code of Ethics Principles reflect professionals’ recognition of their responsibilities to clients, colleagues and employers. The Principles guide the performance and activities of anyone involved in the practice of advice; the concept and intent of these Principles are adapted and enforced on professionals by FPSB through rules of professional conduct.

Principle 1 – Client First

Place the client’s interests first

Placing the client’s interests first is a hallmark of professionalism, requiring the specialist to act honestly and not place personal gain or advantage before the client’s interests.

Principle 2 – Integrity

Provide professional services with integrity.

Integrity requires honesty and candor in all professional matters. Professionals are placed in positions of trust by clients, and the ultimate source of that trust is the specialist’s personal integrity. Allowance can be made for legitimate differences of opinion, but integrity cannot co-exist with deceit or subordination of one’s principles. Integrity requires the specialist to observe both the letter and the spirit of the Code of Ethics.

Principle 3 – Objectivity

Provide professional services objectively.

Objectivity requires intellectual honesty and impartiality. Regardless of the services delivered or the capacity in which a specialist functions, objectivity requires that professionals ensure the integrity of their work, manage conflicts of interest and exercise sound professional judgment.

Principle 4 – Fairness

Be fair and reasonable in all professional relationships. Disclose and manage conflicts of interest.

Fairness requires providing clients what they are due, owed or should expect from a professional relationship, and includes honesty and disclosure of material conflicts of interest. Fairness involves managing one’s own feelings, prejudices and desires to achieve a proper balance of interests. Fairness is treating others in the same manner that you would want to be treated.

Principle 5 – Professionalism

Act in a manner that demonstrates exemplary professional conduct.

Professionalism requires behaving with dignity and showing respect and courtesy to clients, fellow professionals, and others in business-related activities, and complying with appropriate rules, regulations and professional requirements. Professionalism requires the specialist, individually and in cooperation with peers, to enhance and maintain the profession’s public image and its ability to serve the public interest.

Principle 6 – Competence

Maintain the abilities, skills and knowledge necessary to provide professional services competently.

Competence requires obtaining and maintaining an adequate level of abilities, skills and knowledge in the provision of professional services. Competence also includes the wisdom to recognize one’s own limitations and when consultation with other professionals is appropriate or referral to other professionals necessary. Competence requires the specialist to make a continuing commitment to learning and professional improvement.

Principle 7 – Confidentiality

Protect the confidentiality of all client information.

Confidentiality requires that client information be protected and maintained in such a manner that allows access only to those who are authorized. A relationship of trust and confidence with the client can only be built on the understanding that the client’s information will not be disclosed inappropriately.

Principle 8 – Diligence

Provide professional services diligently.

Diligence requires fulfilling professional commitments in a timely and thorough manner and taking due care in delivering professional services.

Are you prepared for a top-tier educational experience provided by the Financial Planning Standards Board Ltd., the organization that sets standards for the financial planning profession globally? Available both online and through instructors like House of Financial Planners, FPSB Ltd.’s investment planning course equips you to enhance your clients’ investment strategies based on their risk profile, financial capacity and constraints.

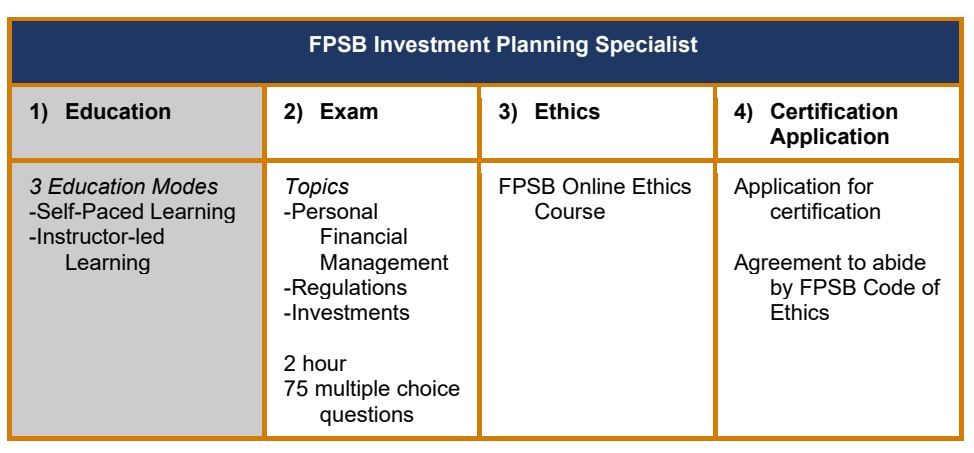

The course teaches you about different types of securities, investment theory and practice, portfolio construction and management, investment strategies and tactics, and securities laws and regulatory compliance. To be recognized by employers, clients, and the public for your knowledge and competency in investment planning, complete the roadmap below to obtain FPSB® Investment Planning Specialist certification in India.

About FPSB Ltd. and FPSB Programs in India

Financial Planning Standards Board Ltd. (FPSB) serves as the global authority for setting standards in financial planning and owns the CFPCM, CERTIFIED FINANCIAL PLANNERCM and , and marks outside the United States. FPSB is delighted to present its Investment Planning Specialist program, one of three pathways to CFP certification in India:

FPSB® Investment Planning Specialist

FPSB® Risk and Estate Planning Specialist

FPSB® Retirement and Tax Planning Specialist

Each certification includes its unique coursework, examination, and credential. Notably, the courses for FPSB pathway certifications contribute to the educational requirements for CFPCM certification in India. Professionals interested in pursuing CFP certification can start by enrolling with FPSB and choosing any of the three pathway certifications, in any sequence. This document will concentrate on the FPSB Investment Planning Specialist certification.

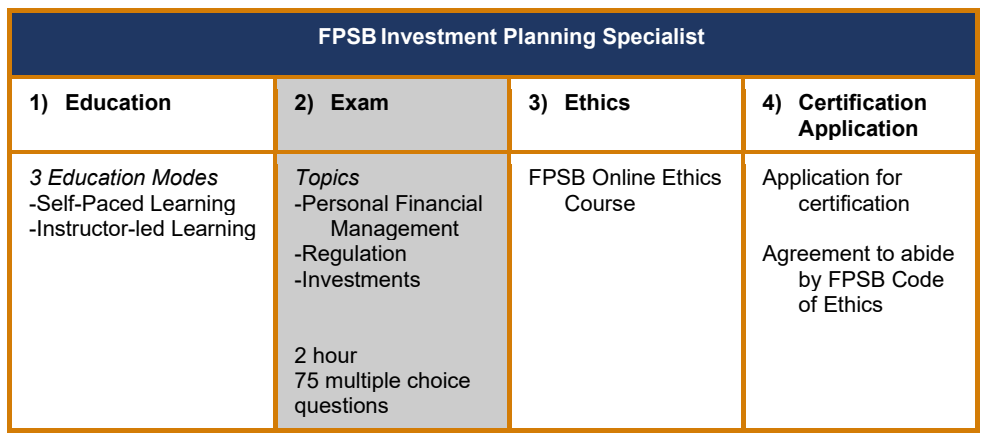

FPSB® Investment Planning Specialist Overview

Take Your Career to the Next Level

Whether completed online or through an instructor like House of Financial Planners, the FPSB® Investment Planning Specialist course details methods for creating strategies and techniques aimed at maximizing a client’s investments, considering their risk profile, financial capacity, and constraints. This course is structured to deepen your understanding of various securities, investment theory and practice, the building and managing of portfolios, investment strategies and approaches, and adherence to securities laws and regulatory compliance.

Steps to Initial Certification

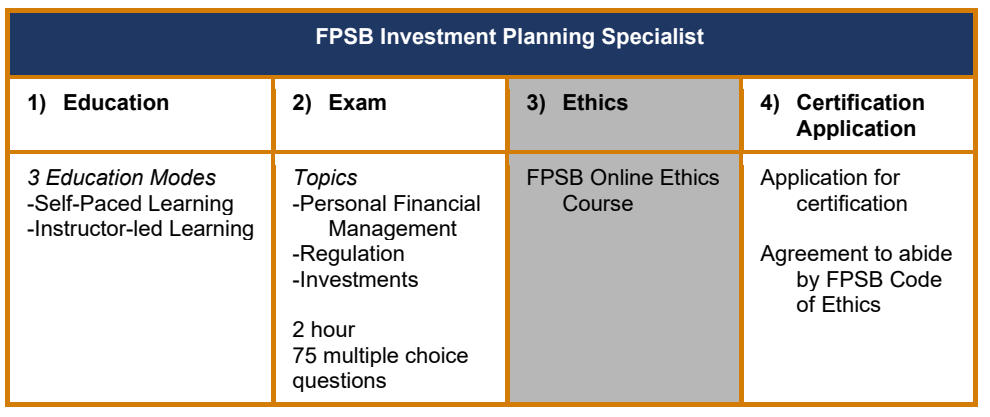

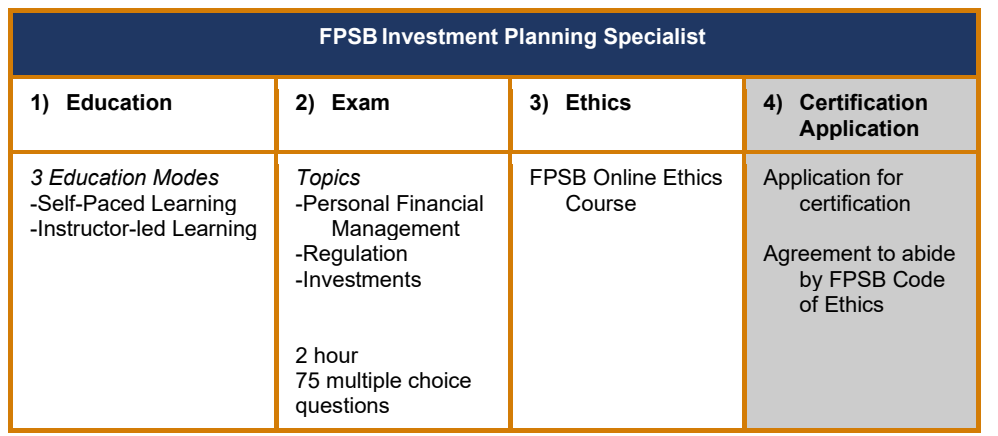

The requirements for FPSB Investment Planning Specialist certification are as follows:

Successfully complete the FPSB Ltd. Ethics Course.

Successfully complete FPSB’s education modules for

Personal Financial Management

Investment Planning and Asset Management

Regulatory Environment, Law and Compliance

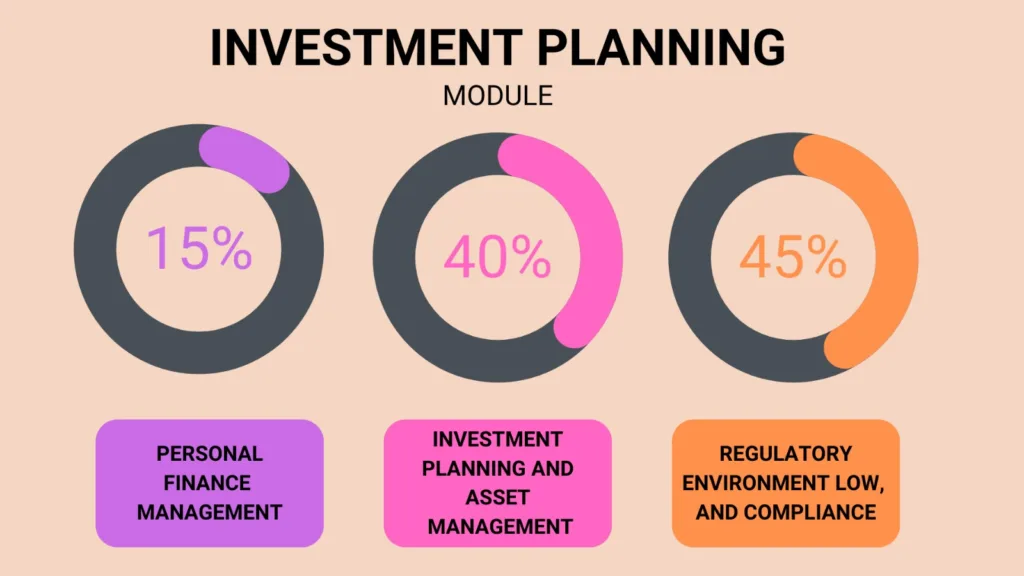

Pass the FPSB Investment Planning Specialist exam, which aligns to the topics identified in the FPSB Investment Planning Specialist Competency Profile.

Complete your certification application, which includes your agreement to comply with FPSB Ltd.’s Code of Ethics and payment of an annual certification fee.

Step 1: Education

Criteria to Register

Candidates must be at least 18 years old and have completed HSC/12th grade (Std XII/HSC) to register with FPSB and start the FPSB Investment Planning Specialist education course. It is required that candidates register with FPSB at least 30 days before registering for the exam.

Period for Course Completion

Individuals are required to finish the FPSB Investment Planning Specialist certification program within three years from their initial registration with FPSB Ltd. and must renew their registration annually. If the program is not completed within three years, FPSB Ltd. will deem the registration invalid. Candidates should evaluate their ability to complete the program within this timeframe before registering.

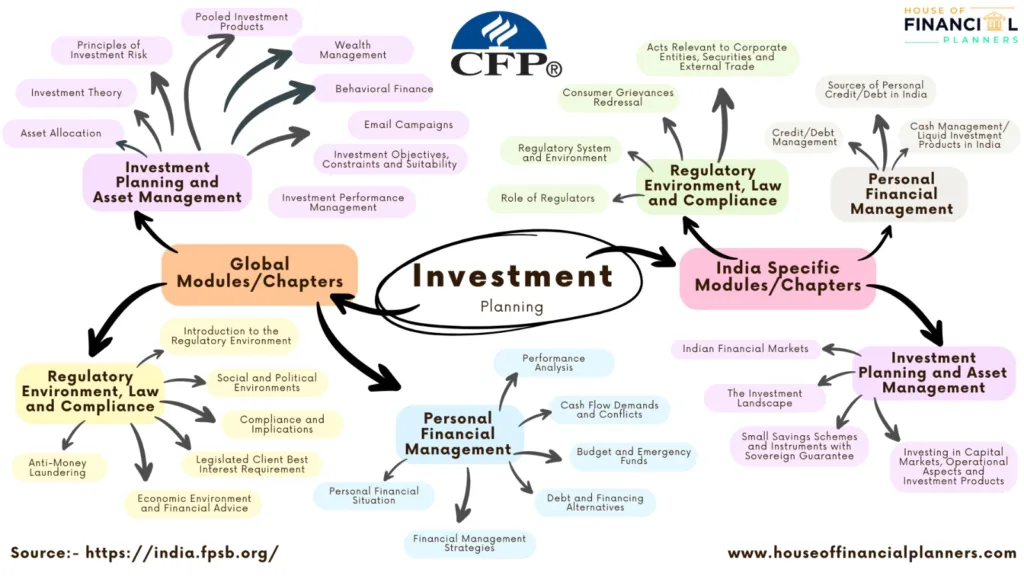

Module

Name and Description

Personal Financial Management

The Personal Financial Management module provides an overview of how to evaluate and collect client information. Candidates will learn how to evaluate investment strategy options and develop financial management strategies based on a client’s unique situation. Candidates will learn how to develop an implementation plan that will provide the client an opportunity to meet his or her financial management goals and objectives.

Investment Planning and Asset Management

The Investment Planning and Asset Management module provides an overview of global and local economic institutions and other factors, such as the stock exchange, asset classes and securities, that impact investment planning as well as principles of investment risk. Candidates will learn various methods of computing expected returns from stocks, bonds and integrated portfolios, including investment risk and valuation ratios Through this module, Candidates will become familiar with the concepts of buying and selling securities, pooled investment products and behavioral finance, and learn how to interview clients to develop a personal risk profile.

Regulatory Environment, Compliance and Law

The Regulatory Environment module provides an overview of key foundational legislation and regulations. Through this module Candidates will become familiar with various regulatory bodies and varying economic, social and political environments. Other fundamental topics covered in the module include anti-money laundering and behavioral finance.

FPSB Ltd. Educational Resources

FPSB Ltd. Will provide program participants with digital textbooks, supplementary post-chapter quizzes, post-module exams, and additional course materials via its online learning platform, MyFPSBlearning. All educational resources provided by FPSB Ltd. are tailored to the FPSB Investment Planning Specialist curriculum. Every candidate, irrespective of their chosen method of study, must acquire these materials.

Education

Candidates may complete the FPSB Investment Planning Specialist education requirement and become eligible to sit for the certification exam in one of three ways:

Self-Paced Education

Candidates who enroll with FPSB and opt for “Self-Paced Learning” will be provided a password to access FPSB’s online learning platform, MyFPSBlearning. There, they can engage with various FPSB learning materials at their preferred pace and evaluate their understanding through quizzes and module tests, enhancing their learning experience. This self-directed educational path is particularly suitable for seasoned investment professionals or motivated individuals who prefer to study according to their own schedules.

*Self-paced learners who do not pass all FPSB Investment Planning Specialist module exams after the two attempts will be asked to pursue the instructor-led path by enrolling with an Authorized Education Provider (AEP). The House of Financial Planners is an authorized education provider of FPSB India.

2. Instructor-Led Education

Candidates seeking a comprehensive educational experience with interactive learning and access to an FPSB Authorized Education Provider should choose the “Instructor-Led Learning” option when registering with FPSB. FPSB Authorized Education Providers deliver both classroom and online learning experiences. Upon registering for instructor-led education with FPSB, individuals will be prompted to choose from among FPSB’s authorized providers, all of which are detailed on the FPSB Ltd. website.

Candidates who opt for FPSB’s instructor-led education can expect to receive the below teaching hours per module.

Step 2. Exam

Upon successfully completing the FPSB Investment Planning Specialist education requirement, either through an FPSB instructor-led course or a self-paced education program, candidates will qualify to take the FPSB Investment Planning Specialist exam.

This exam evaluates the depth of knowledge, skills, and abilities required to obtain the FPSB Investment Planning Specialist credential. It includes tasks such as collection, analysis, and synthesis, which are explained in more detail below. Each question in the exam is mainly based on a specific competency from the FPSB Investment Planning Specialist Competency Profile and may involve combining several competencies to provide a comprehensive assessment.

Exam Overview

75 multiple-choice questions (4 possible answer choices), of which a minimum of 65 questions are potentially scored and up to 10 questions are used to develop future exams.

Computer-based testing format

Duration – two hours

Financial calculators permitted (data must be erased)

There will be two possible marks: correct, with points allotted; or incorrect, for zero points. Candidates will not have points deducted (referred to as ‘negative marking’)

Exam Scoring

The passing point on the FPSB® Investment Planning Specialist exam is set to a level that is what is required for competent practice. Once set, future exams are equated to this same level so that candidates who take the exam one month have the same opportunity to demonstrate their abilities as candidates who take the exam a different month. The level of ability is what is consistent. This means that even if one exam is harder than another, the equating process gives every candidate the same opportunity to pass.

Areas of Practice

The exam will test the following areas of practice, which are also described to in more detail in the FPSB Investment Planning Specialist Competency Profile.

FPSB Investment Planning Specialist Global Areas of Practice

Personal Financial Management

Investment Planning and Asset Management

Regulatory Environment, Law and Compliance

Personal Financial Situation

Investment Objectives, Constraints and Suitability

Introduction to the Regulatory Environment

Cash Flow Demands and Conflicts

Asset Classes and Securities

Legislated ‘Client Best Interest’ Requirement

Budget and Emergency Funds

Pooled Investment Products

Economic Environment and Financial Advice

Debt and Financing Alternatives

Principles of Investment Risk

Social and Political Environments

Financial Management Strategies

Investment Performance Management

Compliance and Implications

Time Value of Money

Investment Theory

Anti-Money Laundering

Asset Allocation

Wealth Management

Behavioral Finance

FPSB Investment Planning Specialist India Specific Areas of Practice

Personal Financial Management

Investment Planning and Asset Management

Regulatory Environment, Law and Compliance

Cash Management/ Liquid Investment Products in India

Indian Financial Markets

Regulatory System and Environment

Sources of Personal Credit/Debt in India

The Investment Landscape

Role of Regulators

Credit/Debt Management

Investing in Capital Markets, Operational Aspects and Investment Products

Acts Relevant to Corporate Entities, Securities and External Trade

Small Savings Schemes and Instruments with Sovereign Guarantee

Consumer Grievances Redressal

Investing in Fixed Income Securities

Other Acts, Statutes and Regulations Relevant to Financial Consumers

Evaluation of Ecosystem and Client Sensitivity in Managing Situations

Regulation of Market Intermediaries in Financial Products

Financial Advisory and Financial Planning

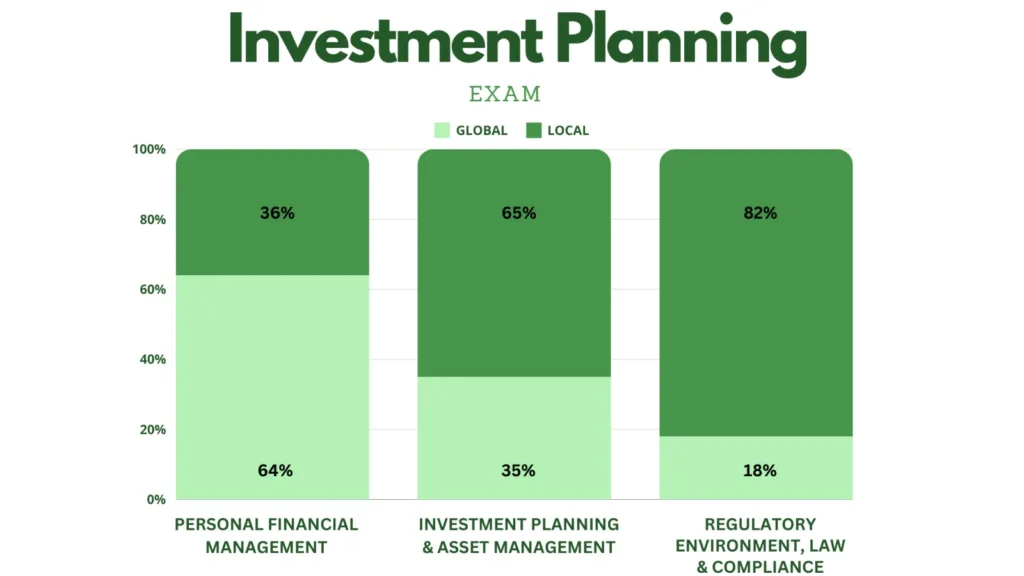

The FPSB Investment Planning Specialist exam will test the knowledge, skills and abilities from the FPSB Investment Planning specialist education modules in the below proportions. However, there will not be specific sections allocated to the modules. Instead, questions relating to each module will appear in no specific order throughout the exam.

Likewise, although the FPSB Investment Planning Specialist textbooks draw a distinction between “global” and “India-specific” education content, exam questions will not be specifically identified as such, and will appear in no specific order throughout the exam.

Difficulty Levels

The FPSB Investment Planning Specialist certification exam is designed to assess knowledge, skills and abilities in the areas of collection, analysis, and synthesis in approximately the following proportions:

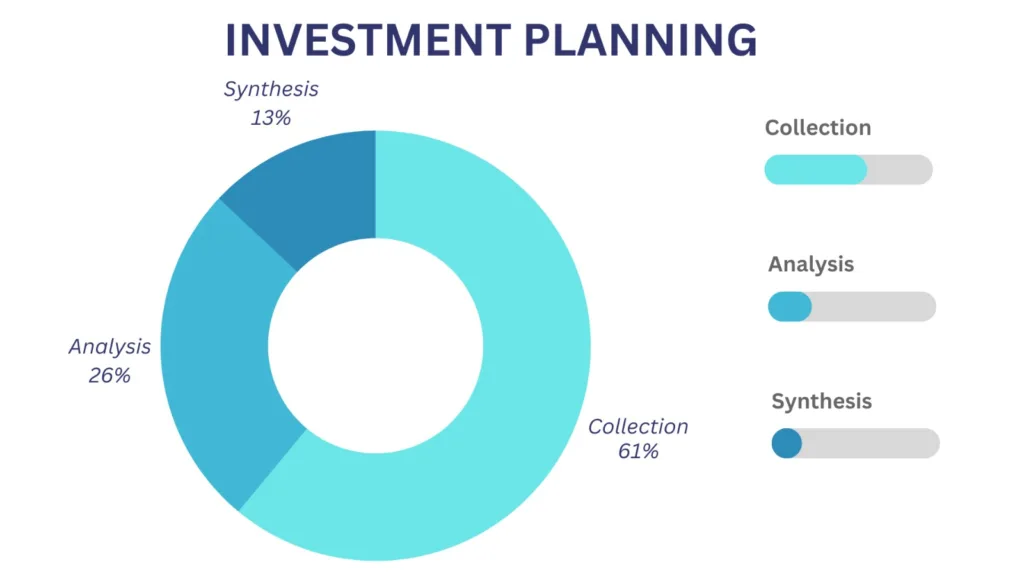

Collection: Gathering information and identifying related facts by making required calculations and arranging client information for analysis. During the collection function, the core competency is to collect both the quantitative and qualitative information required to provide investment advice.

Analysis: considers issues, performs financial analysis and assesses the resulting information to be able to develop strategies for the client. This includes: (1) considering potential opportunities and constraints in developing strategies, and (2) assessing information to develop strategies.

Synthesis: integrates the information needed to develop and evaluate strategies to create an investment plan.

Once submitted, exam results will be reviewed in detail and the Candidate will receive additional determination information. Any appeal must be received no later than 30 days from the intimation of the exam result in LMS or through email. The decision after the appeal is completed will be considered final.

Step 3. Ethics

FPSB requires all individuals complete the FPSB Ethics course shortly after enrolling in the Investment Planning Specialist course. This course, included with the purchase of course materials, is essential as passing it and adhering to the Code of Ethics are prerequisites for obtaining the Investment Planning Specialist certification. The requirement to pass the Ethics course applies only once, even if pursuing multiple Specialist certifications and the CFPCM certification. Conducted online via MyFPSBlearning, the FPSB Ethics Course features interactive, recorded lessons that can be completed in one or several sessions, with periodic knowledge assessments. Once finished, this course fulfills the ethics training requirement for all FPSB Ltd. certifications available in India.

Ethics Attestation

After candidates have passed the FPSB Ethic Course, they must, as part of the FPSB Investment Planning Specialist certification process, attest and agree to abide by the FPSB Code of Ethics.

Introduction

Codes of Ethics

Learning Objectives 1. Explain why financial services professionals should study ethics 2. Describe the difference between values and principles 3. Describe the relationship between ethics and the law 4. Describe a financial services professional 5. Identify characteristics of a professional 6. Evaluate the public perception of the financial services profession

Knowledge Items 1. Why financial services professionals should study ethics 2. The difference between values and principles 3. Ethics and the law 4. Characteristics of a financial services professional 5. Public perception of the financial services profession

Learning Objectives 1. Identify the purposes of codes of ethics 2. Distinguish between the reasonable person standard and the professional practice standard 3. Identify the eight principles of FPSB’s Code of Ethics 4. Apply the principles of FPSB’s Code of Ethics to various case studies and examples 5. Construct a personal code of ethics

Knowledge Items 1. The purpose of a code of ethics 2. Business conduct standards 3. Reasonable person standard 4. Professional practice standard 5. Eight principles of FPSB’s Code of Ethics 6. Personal code of ethics

To maintain the right to use the FPSB Investment Planning Specialist credential, certification holders must maintain their professional skills, knowledge, and abilities through ongoing learning activities.

FPSB Ltd. requires FPSB Investment Planning Specialists to renew their certification annually. To remain certified as an FPSB Investment Planning Specialist certification holders must:

✔ Commit to adhere to FPSB Ltd.’s Code of Ethics and any applicable laws and regulations.

✔ Obtain at least five Continuing Professional Development (CPD) hours/points. All points must be completed before applying for renewal of certification. At least two CPD

hours/points need to directly relate to FPSB Ltd.’s Code of Ethics.

FPSB Coursework as Continuing Professional Development

FPSB Investment Planning Specialists who pursue other Specialist courses are considered to have met their annual CPD requirement through the coursework for FPSB’s other certifications – as proven by registration in the FPSB Risk and Estate Planning Specialist, FPSB Retirement and Tax Planning Specialist, or CFPCM certification programs.

Using your Badge and Certification Name Correctly

FPSB will post guidance on how to correctly identify yourself as an FPSB Investment Planning Specialist. All certification holders will be required to abide by the guidance as part of the FPSB Code of Ethics.

Chapter 3: Acts Relevant to Corporate Entities, Securities and External Trade

Learning Objectives

3-1 Distinguish Acts in India specific to financial sector regulation

Topics

The Companies Act, 2013 (erstwhile 1956)

The Indian Trusts Act, 1882

The Securities Contracts Regulation Act, 1956

The Securities and Exchange Board of India Act, 1992

The Foreign Exchange Management Act, 1999

The Prevention of Money Laundering Act, 2002 (PMLA)

The Insolvency and Bankruptcy Code, 2016 (IBC)

Negotiable Instruments Act, 1883

The Forward Contracts Regulation Act, 1952

The Indian Contract Act, 1872The Indian Partnership Act, 1932

The Limited Liability Partnership Act, 2008

Chapter 4: Consumer Grievances Redressal

Learning Objectives

4-1 Understand consumer grievances redressal under various regulators

4-2 Distinguish nuances of comprehensive consumer empowerment in the digital era

Topics

Redress in Banking – The Banking Ombudsman Scheme 2006 (amended July 1, 2017)

Investor Grievance Redress Mechanism – SEBI Complaints Redress System (SCORES) platform

Insurance Ombudsman Scheme

Stipendiary Ombudsman – PFRDA

The Consumer Protection Act, 2019 (new act)

Chapter 5: Other Acts, Statutes and Regulations Relevant to Financial Consumers

Learning Objectives

5-1 Understand other Acts, Statutes and Regulations impacting financial consumers

Topics

Right to Information Act, 2005 RTI)

SEBI (Disclosure and Investor Protection) Guidelines, 2000 (DIP)

IRDAI (Protection of Policyholders’ Interests) Regulations, 2017

Chapter 6: Regulation of Market Intermediaries in Financial Products

Learning Objectives

6-1 Compare regulations of market intermediaries in financial products

Topics

SEBI (Intermediaries) Regulations, 2008

SEBI (Investment Advisers) Regulations, 2013

SEBI (Self-Regulatory Organizations) Regulations, 2004

PFRDA Retirement Adviser) Regulations, 2016

PFRDA (Point of Presence) Regulations, 2015

IRDA (Licensing of Insurance Agents) Regulations, 200

FPSB Certification Code of Ethics (for all FPSB certifications)

FPSB LTD. CODE OF ETHICS

Observing the highest ethical and professional standards allows professionals to serve the interests of clients and promote the profession for the benefit of society. As part of their commitment, professionals should provide appropriate disclosures and comply with ethical standards when delivering advice to clients. FPSB has incorporated ethical behavior and judgment, and compliance with ethical standards, into its global standards for professionals. To ensure these obligations are understood, FPSB incorporates ethical standards into its certification requirements.

FPSB’s Code of Ethics Principles are statements expressing in general terms the ethical standards that professionals should adhere to in their professional activities. The comments following each Principle further explain the intent of the Principle. The Principles are aspirational and are intended to provide guidance for professionals on appropriate and acceptable professional behavior.

FPSB’s Code of Ethics Principles reflect professionals’ recognition of their responsibilities to clients, colleagues and employers. The Principles guide the performance and activities of anyone involved in the practice of advice; the concept and intent of these Principles are adapted and enforced on professionals by FPSB through rules of professional conduct.

Principle 1 – Client First

Place the client’s interests first

Placing the client’s interests first is a hallmark of professionalism, requiring the specialist to act honestly and not place personal gain or advantage before the client’s interests.

Principle 2 – Integrity

Provide professional services with integrity.

Integrity requires honesty and candor in all professional matters. Professionals are placed in positions of trust by clients, and the ultimate source of that trust is the specialist’s personal integrity. Allowance can be made for legitimate differences of opinion, but integrity cannot co-exist with deceit or subordination of one’s principles. Integrity requires the specialist to observe both the letter and the spirit of the Code of Ethics.

Principle 3 – Objectivity

Provide professional services objectively.

Objectivity requires intellectual honesty and impartiality. Regardless of the services delivered or the capacity in which a specialist functions, objectivity requires that professionals ensure the integrity of their work, manage conflicts of interest and exercise sound professional judgment.

Principle 4 – Fairness

Be fair and reasonable in all professional relationships. Disclose and manage conflicts of interest.

Fairness requires providing clients what they are due, owed or should expect from a professional relationship, and includes honesty and disclosure of material conflicts of interest. Fairness involves managing one’s own feelings, prejudices and desires to achieve a proper balance of interests. Fairness is treating others in the same manner that you would want to be treated.

Principle 5 – Professionalism

Act in a manner that demonstrates exemplary professional conduct.

Professionalism requires behaving with dignity and showing respect and courtesy to clients, fellow professionals, and others in business-related activities, and complying with appropriate rules, regulations and professional requirements. Professionalism requires the specialist, individually and in cooperation with peers, to enhance and maintain the profession’s public image and its ability to serve the public interest.

Principle 6 – Competence

Maintain the abilities, skills and knowledge necessary to provide professional services competently.

Competence requires obtaining and maintaining an adequate level of abilities, skills and knowledge in the provision of professional services. Competence also includes the wisdom to recognize one’s own limitations and when consultation with other professionals is appropriate or referral to other professionals necessary. Competence requires the specialist to make a continuing commitment to learning and professional improvement.

Principle 7 – Confidentiality

Protect the confidentiality of all client information.

Confidentiality requires that client information be protected and maintained in such a manner that allows access only to those who are authorized. A relationship of trust and confidence with the client can only be built on the understanding that the client’s information will not be disclosed inappropriately.

Principle 8 – Diligence

Provide professional services diligently.

Diligence requires fulfilling professional commitments in a timely and thorough manner and taking due care in delivering professional services.

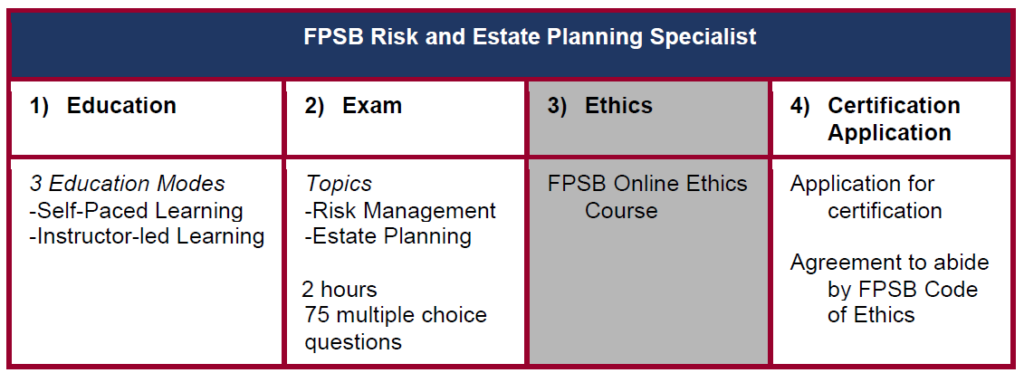

Are you prepared for a premier learning experience provided by the Financial Planning Standards Board Ltd., the global authority setting standards in the financial planning industry? Whether taken online or through an instructor like House of Financial Planners, FPSB Ltd.’s risk and estate planning course equips you to devise strategies to minimize your clients’ financial risks and effectively manage their accumulated assets.

The course teaches you to evaluate your clients’ legal, tax, financial, and insurance positions, and the impacts of non-financial issues, to guide clients to conserve and transfer wealth consistent with client goals. To be recognized by employers, clients, and the public for your knowledge and competency in retirement and tax planning, complete the roadmap below to obtain FPSB® Risk and Estate Planning Specialist certification in India.

About FPSB Ltd. and FPSB Programs in India

Financial Planning Standards Board Ltd. (FPSB) serves as the global authority for setting standards in financial planning and is the proprietor of the CFPCM, CERTIFIED FINANCIAL PLANNERCMand, and marks outside the United States. FPSB proudly offers its Risk and Estate Planning Specialist program, which is one of three pathways to achieving CFP certification in India:

FPSB® Investment Planning Specialist

FPSB® Retirement and Tax Planning Specialist

FPSB® Risk and Estate Planning Specialist

Each certification pathway includes its specific coursework, examination, and credential. Notably, completing these pathway courses also counts towards the educational requirements for CFPCM certification in India. Professionals interested in pursuing CFP certification can start by enrolling with FPSB and choosing any of the three pathway certifications, in any sequence. This document will concentrate on the FPSB Risk and Estate Planning Specialist certification.

FPSB® Risk and Estate Planning Specialist Overview.

Take Your Career to the Next Level

The FPSB® Risk and Estate Planning Specialist course equips you to create strategies that manage clients’ financial exposure arising from personal risks and assists clients in preserving and distributing their accumulated assets.

This course trains you to assess your clients’ legal, tax, financial, and insurance positions, as well as the impacts of non-financial factors, guiding them to protect and transfer wealth in alignment with their objectives. To gain acknowledgment from employers, clients, and the public for your advanced skills and knowledge in risk and estate planning, follow the outlined steps to secure the FPSB® Risk and Estate Planning Specialist certification in India.

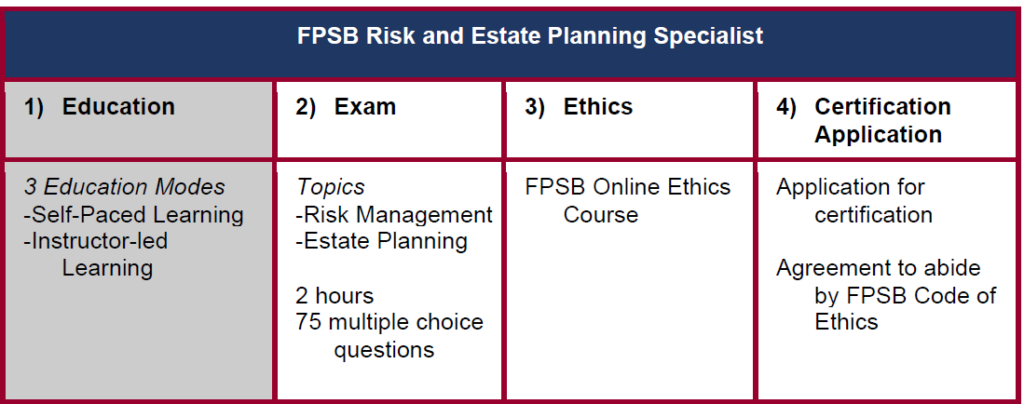

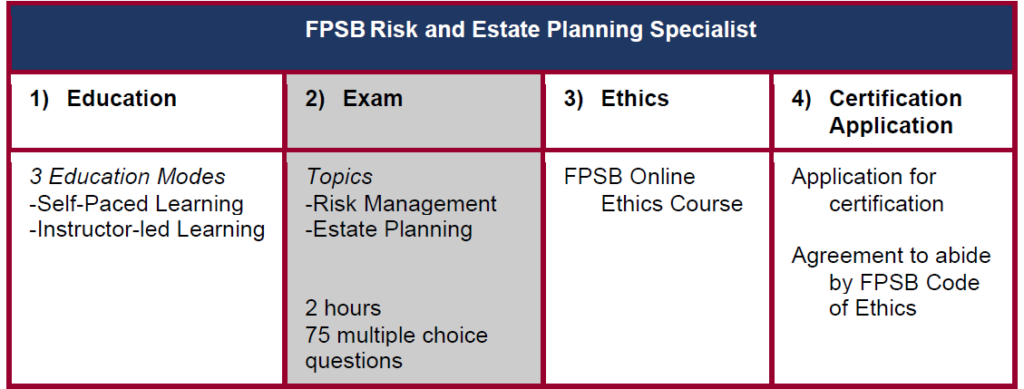

Steps to Initial Certification

The requirements for FPSB Risk and Estate Planning Specialist certification are as follows:

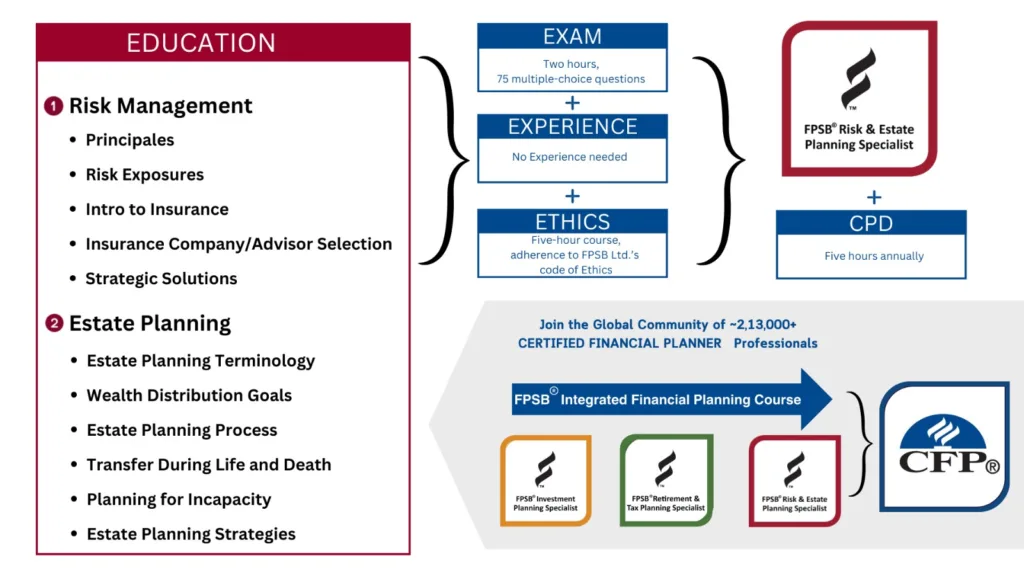

Successfully complete the FPSB Ltd. Ethics Course.

Pass the FPSB Risk and Estate Planning Specialist Exam, which aligns with the topics identified in the FPSB Risk and Estate Planning Specialist Competency Profile

Complete your Certification Application, which includes your agreement to comply with FPSB Ltd.’s Code of Ethics and payment of an annual certification fee.

Step 1: Education

Criteria to Register

Candidates must be at least 18 years old and have completed HSC/12th grade (Std XII/HSC) to register with FPSB and start the FPSB Risk and Estate Planning Specialist education course. It is required that candidates register with FPSB at least 30 days before registering for the exam.

Period for Course Completion

Individuals must complete the FPSB Risk and Estate Planning Specialist certification program within three years of their initial registration with FPSB Ltd., and they are required to renew their registration annually. If the program is not completed within three years, FPSB Ltd. will deem the registration invalid. Candidates should evaluate their ability to complete the program within this timeframe before registering.

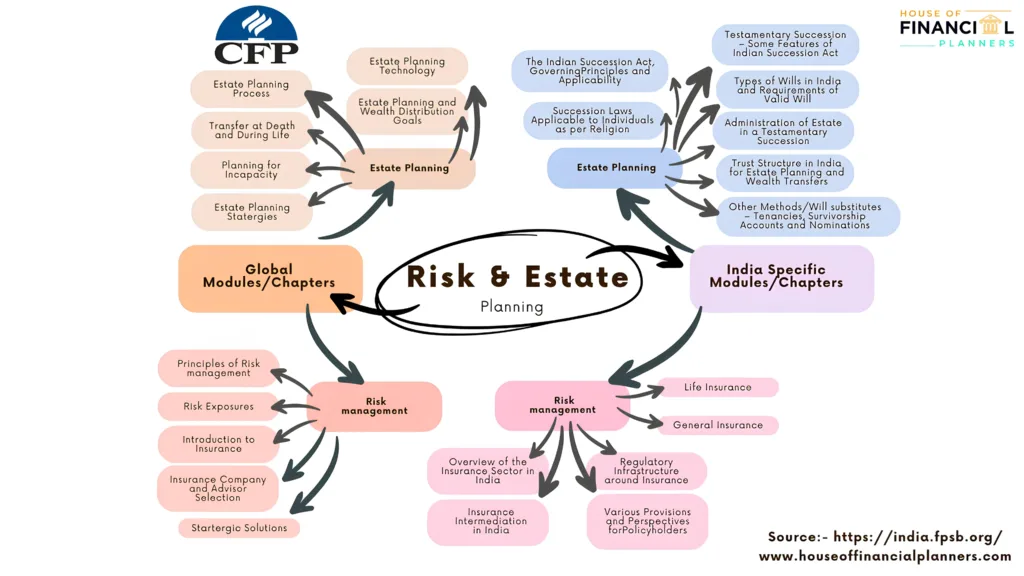

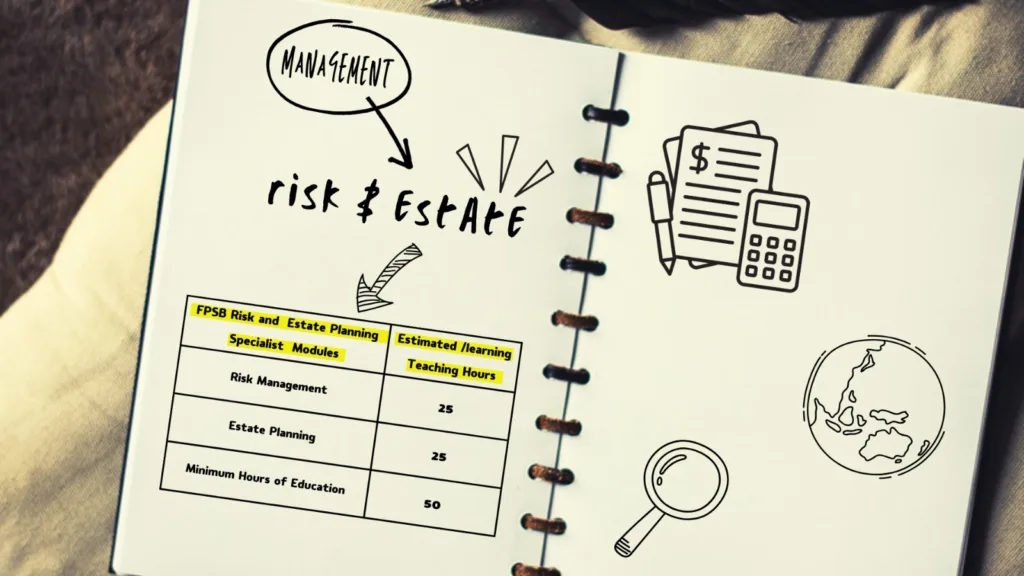

Module

Name and Description

Risk Management